Humans are anchored in the present, which makes it easy to underestimate both how profoundly the past has changed and how radically the future will. The digital world is in the midst of a structural transformation that will reshape institutions, industries, and daily life. Yet it is important to remember that most economic value—and most human experience—still resides in the physical world.

Consider aviation. Paper tickets have long since disappeared, but the core experience of flying has changed little. Jumbo jets entered commercial service in 1970, and more than five decades later the passenger experience is broadly familiar, even if the supporting infrastructure has expanded beyond recognition to accommodate exponential growth in air travel. Extend the lens further: compared with humans living 5,500 years ago, our DNA has barely shifted. Our technological power has advanced to the point where we can materially damage the planet; our biological foundations have not.

Insurance sits squarely at this intersection between digital process and physical consequence. Insurance is a promise—one that can be transacted, priced, and serviced in digital form. But when that promise is called upon, the impact is usually tangible: damaged property, injured people, disrupted businesses. Artificial intelligence (AI) will undoubtedly reshape how that promise is underwritten, distributed, and fulfilled. However, the underlying nature of the promise itself remains constant.

AI represents a genuine discontinuity for the insurance industry, yet many of its fundamentals will persist. The shift from a paper-based industry over the past 50-60 years to today’s digitally enabled ecosystem arguably constituted a larger structural transformation than AI alone is likely to deliver. What differs now is velocity. Five decades ago, every high street hosted multiple insurance brokers; today, that distribution model has largely vanished. The compression of change cycles is the defining feature of the current era.

The AI wave will move through the industry rapidly and will be measured in years, not decades. As with the introduction of the iPhone and other general-purpose technologies, the initial phase will be turbulent and disruptive. Over time, adoption will normalize, competitive positions will solidify, and the identities of winners and losers will become clear.

Darwinian shorthand often invokes “survival of the fittest,” but a more precise formulation is survival of the adaptable. In periods of structural upheaval, adaptability—organizational, cultural, and technological—is the critical differentiator.

In commercial insurance over the past decade, the rise of Managing General Agents (MGAs) illustrates this principle. Enabled by technology, MGAs have driven product and distribution innovation at a pace that large insurers—constrained by scale, legacy systems, and institutional inertia—have struggled to match. Their relative lack of scale has often been an advantage, allowing faster experimentation and deployment. Meanwhile, many insurers have increasingly functioned as capital providers, with underwriting expertise migrating into specialist vehicles. AI is likely to accelerate this disaggregation.

Yet while methods may change, the identity of value-capturing actors may not. In any promise-based industry, control of the customer relationship is decisive.

In UK personal lines, customer ownership has shifted repeatedly

Historically, high street personal lines brokers controlled distribution. When Peter Wood launched Direct Line, he disrupted that model—so profoundly that he sought backing from Royal Bank of Scotland rather than traditional industry players. Later, with the growth of the internet and broadband connectivity, price comparison websites consolidated control over customer acquisition, capturing a disproportionate share of the value chain. AI now poses a credible threat to this oligopoly, signaling the beginning of another contest for customer ownership in personal lines.

Commercial insurance presents a contrasting picture

Despite substantial technological evolution, the commercial broker has continued to own the client relationship and, consequently, to command a significant share of the economic surplus. Insurers “manufacture” the risk product, but brokers frequently capture superior economics through commissions, profit shares, overriders, and work-transfer payments. Clients typically focus on the premium charged by the insurer rather than the broker’s total extraction from the value pool, reinforcing this structure.

AI will alter how commercial brokers operate—enhancing placement efficiency, risk analysis, and client servicing. However, unless it meaningfully disrupts the broker-client relationship, there is little evidence that it will displace brokers from their structurally advantaged position. If anything, adaptable brokers, distributors, and MGAs may expand their share of the value chain. Their relative agility—often a function of smaller scale—positions them well to navigate and exploit a period of unprecedented technological change.

Get the full market analysis

Watch for the upcoming 2025 UK Insurance Distribution M&A Market Report for exclusive data on the M&A transactions, trends, buyers and key insights shaping the future of the industry.

After the multi-year low for insurance distribution sector mergers and acquisitions (M&A) in 2025, as measured by both deal volume and value, there were tentative signs of a pickup in activity in January, as several notable new transactions were announced. Although eight new deals in a month is still below the long-term monthly average (9.6), in January 2025 there were only four deals. More significant was the nature and size of new deals during the month, which included new direct private equity (PE) investment into a commercial broking consolidation vehicle, a network deal, and a major transaction involving an overseas acquirer. While one month is not enough to start making predictions for the year ahead, it is a positive start to the year.

M&A Market Update

There were eight new deals in January, which was twice as many as in January 2025. It is far too early in the year to divine any trends from this. Because the deal numbers are so small this early in the year, the deal numbers should be more statistically significant by the Spring and the charts at that time will show the percentage splits around retail vs. specialty and PE-backed capital vs. private capital, percentage of overseas buyers etc. The charts below look back at the overall value of sector M&A in 2025, which MarshBerry has not previously published. Our next annual M&A and market structure review, which will be available in early March, will include this data, as well as a more detailed analysis and commentary on the 2025 numbers than we have space for here.

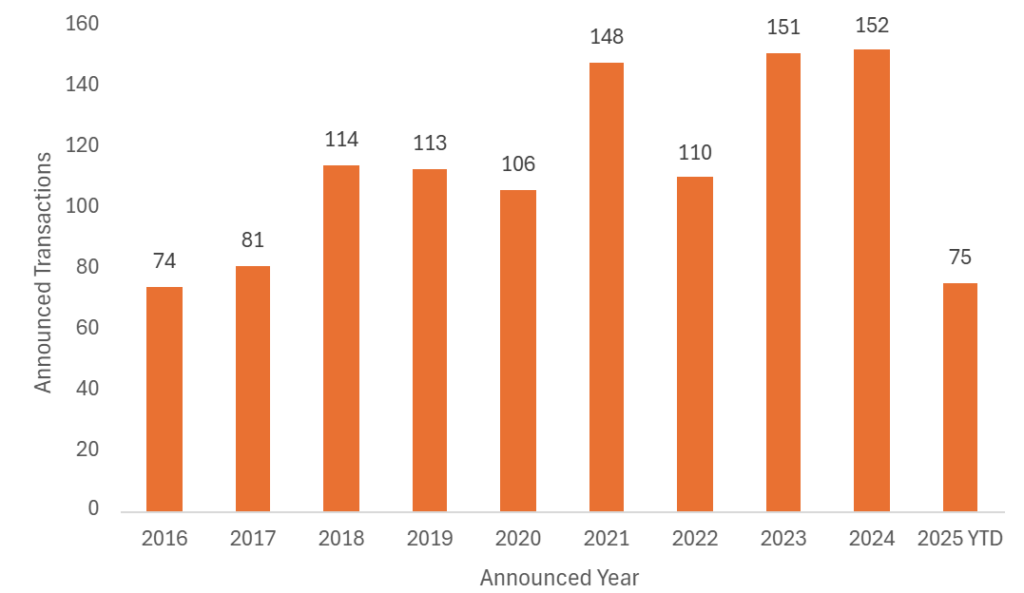

Number of Announced UK Insurance Distribution M&A Transactions, since 2016

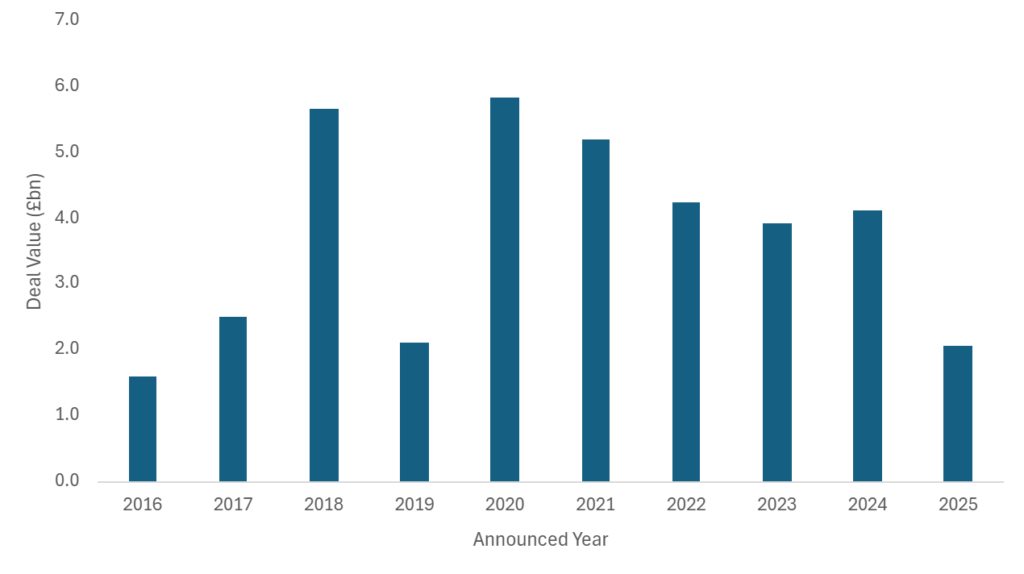

The value of sector M&A decreased in 2025

Not only were there fewer deals in 2025, but the average deal size also reduced, as it has for a number of years. Although there were a handful of large transactions in the year, mainly involving PE investment in both primary and secondary buyout deals (Seventeen Group, BPL, Jensten Group, JMG Group), there were also none of the ‘mega’ deals (>£1bn) that can really move the numbers in a given year. The result was that aggregate deal value across the 99 deals announced in 2025 was just over £2 billion, the lowest total since 2016 and around half the average deal value that sector M&A has delivered over the past three years. Of course, one or two large deals could have substantially changed this – think PIB Group’s aborted deal with Gallagher at a rumoured valuation of more than £3 billion – and so it is a poor barometer of the level of underlying sector M&A activity, but it does reinforce the fact that 2025 saw a marked pullback in deal activity. In January 2026 there has already been one deal valued at above £100m (AUB Group’s £219m deal for Prestige) and as sector consolidation results in bigger and bigger groups that are typically backed by PE investors who are by their very nature only temporary owners, the overall value of sector M&A will remain concentrated across a small number of very large deals.

Deal Value of announced UK Insurance Distribution M&A (all deals) 2016-2025 – in £bn

Will January set the tone for the rest of 2026?

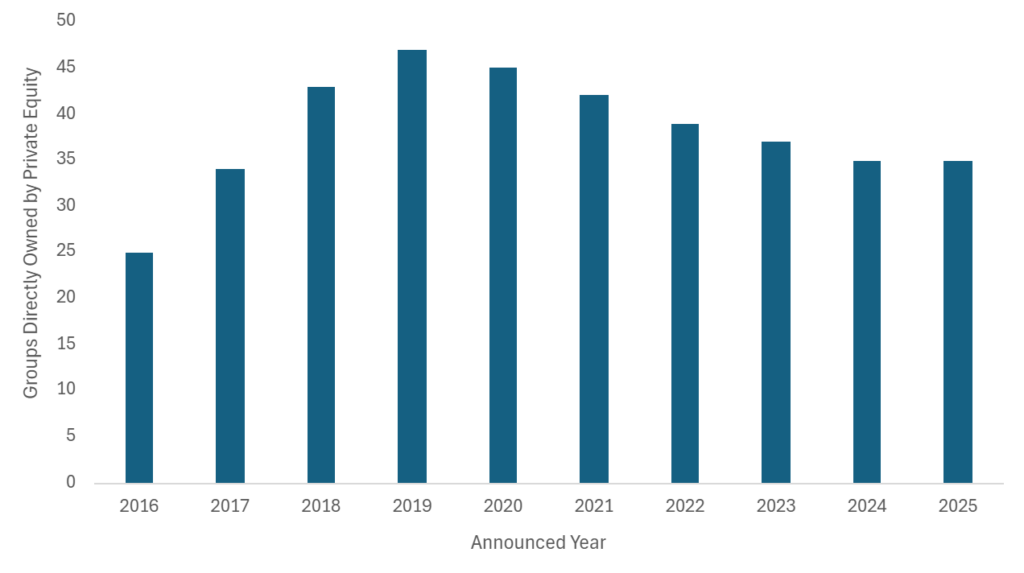

January’s deals highlight two themes that were in evidence throughout 2025 and are set to continue in 2026. Inflexion’s investment in Ascend brings further fresh capital to the sector to support domestic consolidation in commercial broking, and will further increase competition amongst a buyer universe chasing a decreasing number of privately-held commercial broking targets of scale. Capital Z’s exit of Prestige to a trade buyer, AUB Group, sees PE capital coming out of the sector, but again highlights the attractiveness of the UK market to larger overseas groups with an international growth strategy. There were 35 insurance distribution groups directly held by PE investors at the end of 2025, the same number as at the beginning of the year (following five new investments and five divestments during 2025). Several of these will be put up for sale in 2026, with buyer interest expected to come from PE (i.e., secondary deals), other domestic consolidators, and overseas trade/strategic. Watch this space.

No. of UK insurance distribution groups directly owned by Private Equity

What to expect in 2026

MarshBerry has previously noted that several of the factors that suppressed deal volumes in 2025 – a lack of supply of mid-sized targets, softening rates removing an industry tailwind (and in turn dampening valuations of the publicly listed broking groups in the U.S.), and macroeconomic uncertainties – will not reverse overnight, and as such there are few immediate catalysts for an immediate uptick in M&A volumes. It is not all doom and gloom however. Capital to support industry consolidation remains plentiful, with recent new PE investment-backed buyers focused on domestic M&A. The UK remains an attractive market on the radar of many overseas groups. Industry fragmentation, at least at the smaller end, remains high, with ageing owners that will need to sell. And new businesses continue to be formed – particularly in the specialty segment, where the rise and rise of MGAs (Managing General Agents) shows few signs of slowing. Deal activity is unlikely to bounce back to 2023/24 levels in 2026, but sector M&A isn’t going away.

The increased caution that characterised 2025 is likely to persist in 2026, with PE investors that have bought in at high multiples remaining nervous about their ability to generate hoped-for returns in the current environment. Public market valuations will trickle down to impact deal pricing for brokers further down the chain. Reduced valuations will impact staff equity owners, which risks weakening the ‘glue’ that can hold some groups together. The recent failure of some larger groups that had not fully integrated acquisitions to attain premium valuations on their sales will continue to push owners and management teams to focus more on integration, and in turn may encourage a more selective approach to M&A.

MarshBerry will continue to monitor and report on these trends, both in the UK and across our markets. If you would like to discuss the changing M&A environment or speak to an expert about your own business, we would love to hear from you.

Notable transactions (January 2026):

- Mid-market PE firm Inflexion, which has previously backed both Bollington Wilson and DR&P, announced it would be again investing in the UK commercial broking segment with ambitious plans to build out a new broker platform, using Ascend Broking Group as an anchor investment.

- Clear Group announced two new deals in the month, adding veterinary sector specialist Shire Insurance Services which will become part of its retail division, and Gauntlet, comprising Gauntlet Retail Brokers and The Gauntlet AR Network, a principal for Appointed Rep insurance brokers that it is envisaged will help develop Clear-owned network Brokerbility.

- Australian-listed AUB Group, which already owns Tysers and Movo in the UK, announced the acquisition of PIHL Holdings, the parent company of Prestige Insurance, in a deal valued at £219 million. Prestige operates across broking, MGA business and technology, across several brands and multiple locations. It will serve as AUB’s principal UK retail broking platform. The business has been backed by specialist PE investor Capital Z Partners since 2018.

Other transactions (January 2026):

- Nexus Underwriting, part of Brown & Brown (Europe) announced the acquisition of Sure Insurance Services, a specialist in cover for medical tourism.

- Partners&, one of the Top 10 most active buyers in 2025, continued its recent run of deals with the acquisition of STP Risk Solutions, a commercial broker in Hull.

- Specialist Risk Group announced the acquisition of commercial broker Kennett Insurance & Risk Management, also in Hull. SRG acquired the business from WF Risk Group, from whom they previously acquired Generation Underwriting in a deal announced in 2025.

- It was reported (by Matt McColl) that Matt McColl, the founder and CEO of recycling and waste specialist Raw Material Cover had reached an agreement to acquire Lothbury UK, the Lloyd’s broker.

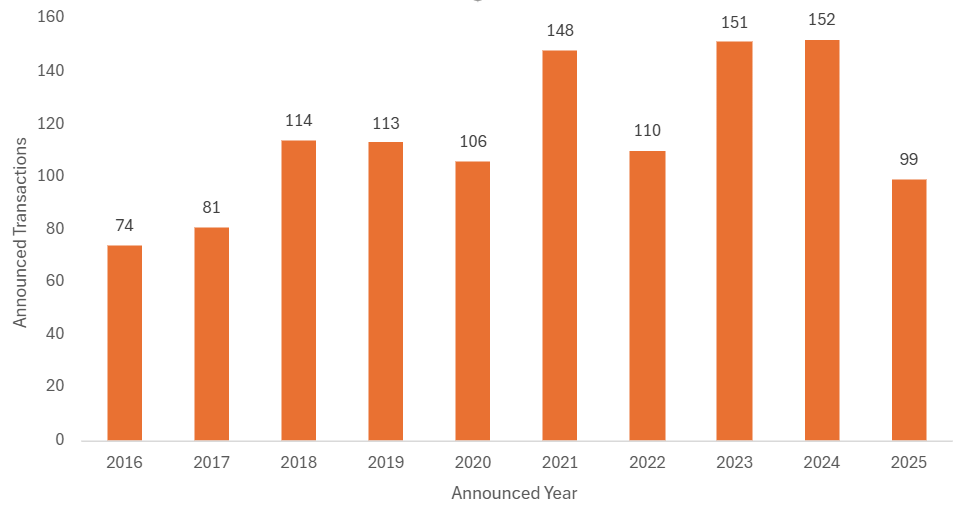

December is a ‘short’ month in terms of business days, and in the UK, there is no tax-driven motivation to close deals by year end. Historically, December has been no less active than any other month for insurance distribution mergers and acquisitions (M&A), with an average of more than eight deals a month over the past decade. However, December 2025 saw only four new deals, making it (jointly) the quietest month of 2025 for M&A, and the quietest December since 2016. It means the UK ended the year with 99 deals announced, just shy of the 100 figure that the month-on-month deal count has been broadly tracking towards throughout 2025. It also marked the first time since 2017 that the total number of sector deals in a year has not exceeded 100.

M&A Market Update

The small number of new deals announced in December left the total for the year just shy of 100, rounding out a slow year for sector M&A. MarshBerry will be publishing its annual review of sector M&A in the spring. This review will detail who sold and why, as well as looking at the overall value of M&A, including using headcount analysis to consider the changing pace of overall sector consolidation. (Spoiler Alert: both have fallen substantially.) This month’s M&A update is just a short summary of how the year ended, with a few suggestions as to why 2025 has seen such a precipitous decrease in the number of UK deals.

Total Volume of Announced UK Insurance Distribution M&A, Annual

A quiet Q4 for sector M&A

With only 22 announced deals in Q4, the last quarter of 2025 has been the quietest Q4 for sector M&A since 2016. This is in spite of a number of JMG Group’s 2025 deals falling into the quarter, as well continued activity from consistently active buyers including Partners&, The Broker Investment Group and Jensten Group. But as MarshBerry has remarked before, the story of 2025 has been of a year in which many of the most active buyers of the past 5-10 years have done significantly less M&A – Ardonagh, Brown & Brown, PIB Group, Clear, Gallagher and Seventeen Group have all been noticeably quieter over the past 12 months, at least in the UK.

But why has sector M&A fallen so rapidly? And why have the deal sizes declined? Of the 99 deals in 2025, more than half have involved a target employing fewer than 10 staff, and there were only five deals with a value of more than £100 million, the lowest since 2019. Some of this relates to supply: the fact is that there are significantly fewer mid-sized targets for consolidators to go after, but there are also demand-side explanations.

The softening rate environment has removed a multi-year tailwind from the sector, impacting organic growth. As a result, some of the larger private equity (PE)-owned businesses are having difficulties securing high-multiple exits. While valuations of publicly-traded brokers have declined over the past three quarters, with a trickle down impact on the valuations further down the food chain. Creating lasting value has become more difficult, which has introduced increased caution around acquisitions and renewed scepticism of the “pile ‘em high” M&A strategies that have characterised the recent record-breaking years of deal activity.

What will sector M&A activity in 2026 look like?

There are arguably no immediate catalysts that will likely push deal activity up to 2023/24 levels for the foreseeable future. Softening rates, debt costs that are still historically high and general macroeconomic nervousness are unlikely to fade away quickly. On the supply side, new broker and MGA (Managing General Agent) formations coming to market in 2026 won’t even scratch the surface in terms of filling demand. But on the plus side, the sector still has plenty of capital waiting to be deployed in M&A. Three UK commercial broking consolidators took on new PE capital in 2025. Overseas interest in UK insurance distribution remains buoyant (there were 15 unique overseas buyers of businesses in 2025, of which four were acquiring in the UK for the first time) and is not limited to North America. And the factors that make insurance distribution such an attractive, resilient and enduring sector – as well as the demonstrable value that a well-executed acquisitive growth strategy can deliver – are not going away.

Notable transactions (December 2025):

- In another example of a carrier divesting a distribution business, Canopius announced that its tech-led MGA Vave has been acquired by Acrisure, where it will become part of Acrisure Underwriting. Vave is a UK-headquartered MGA that uses APIs to write mainly cat-exposed business in the U.S.

- Clear Group announced that it had continued to extend its geographical reach with its first acquisition in Scotland, where it has added Cairn Corporate, a commercial broker based in Fife.

- Peter Cullum’s The Broker Investment Group (TBIG), via The Needham Group, acquired 100% of Black Lion Broking Services, a commercial broker in Surrey. TBIG has been among the most active UK buyers during the year, with only JMG Group having announced more broking deals in 2025.

Other transactions (December 2025):

- In the second deal of the month involving a Scottish target, Bain-backed Jensten Group acquired Broker One, a commercial broker in Glasgow.

* Note that the full year 2025 figure of 99 includes a small number of formally unannounced deals identified via Companies House PSC notifications and so in the public domain. We will be publishing a listing of all deals in the year involving a target reporting 10 or more staff in our annual review, available in early Spring.

Every January, the local gym fills up with new faces. For many, it’s a triumph of hope over experience. However, by mid-February, life on the mats is back to normal. It’s a testament for how sustained effort—not good intentions—is key to delivering results.

The same is true in business.

Sustained effort beats short-term momentum

We recently caught up with a MarshBerry client who had smashed the earn-out in a deal. Interestingly, the principal chose not to see it through to the end. Instead, he had taken the opportunity that selling had provided and pursued a new career while he still had the enthusiasm and energy (he was well short of retirement age).

So, what made this deal such a success? Nothing radical. For the last decade, the business had done the following consistently and to the highest standards:

- Invested in staff;

- Invested in client relationships;

- Invested in systems, processes and so much more.

What drives a smooth and successful sale

Many owners think the hard work ends when heads of terms are signed. In reality, that’s just the beginning. Heads of terms set out the broad commercial agreement and give the buyer exclusivity to complete due diligence, legal documentation, and obtain FCA approval. But due diligence, which delves into the past to ensure there are not undiscovered issues in the future, is exhaustive and the legal complexities are considerable.

In this particular transaction, the buyer of the business (and they have bought a great many businesses) said they have never had the due diligence process run so smoothly. Everything was there when they asked for it, everything was documented and in good order. Whilst our client worked hard to deliver what was asked, the ability to deliver it so effectively reflected the exemplary standards that had been in place for many years.

Long-term discipline defines post-sale success

So, what will the new year bring for this client? Like the gym, results come from sustained effort. Great businesses aren’t built overnight—they’re the product of years of investment and care. For our client, that meant leaving the business in the hands of the next generation, confident they would continue to deliver. The performance of a business post sale is the acid test of the many years of work before.

MarshBerry won’t be involved in their next venture (it’s outside financial services) but we’re certain it will succeed. Why? Because the same exacting standards that built their first business will build the next.

We are always keen to talk to business owners many years before they sell, as that is when much of what makes for a successful sale is being put in place. Being involved in the journey helps us to ensure that for our clients the final destination is optimal.

As 2025 draws to a close, the insurance broking sector finds itself at a subtle but meaningful turning point. Merger and acquisition (M&A) deal activity remained solid, capital stayed available and investor appetite did not disappear. Yet beneath the surface, the growth dynamics that had supported the industry for much of the past decade began to change. This was the year in which insurance broking could no longer rely on favourable market conditions alone and was forced to confront more structural questions around growth, positioning and long-term value creation.

The end of easy organic growth

One of the defining shifts in 2025 was the move away from a prolonged hard market towards more mixed and gradually softer conditions across the insurance landscape. After many years of strong pricing, additional capacity and a more stable loss experience began to slow rate momentum in areas such as liability and property. Personal lines, particularly motor, continued to face pricing pressure, while specialty lines remained volatile.

This shift made growth more demanding. With pricing no longer lifting results across the board, revenue growth increasingly depended on winning new clients, deepening relationships and broadening service offerings. Firms with a clear sector focus, strong commercial discipline and active sales cultures were better equipped to adapt.

Insurance Broker M&A remained active, but more deliberate

Despite broader market shifts, M&A activity in insurance broking remained resilient throughout 2025, especially across continental Europe. Deal volumes continued at a solid pace, supported by a broad base of strategic buyers and financial investors with capital to deploy. In contrast, the UK market saw noticeably fewer announced transactions than in recent years, with deal counts down substantially compared with 2023 and 2024 as the domestic consolidation wave matured and available targets thinned.

Buyer behaviour also evolved. Acquisitions were increasingly targeted at strengthening specialty capabilities, building regional density and underpinning defined platform strategies rather than simply accelerating scale. Greater weight was placed on earnings durability, client retention and integration readiness, leading to more selective processes and clearer differentiation between assets.

M&A remained active, but more deliberate

Despite broader market shifts, M&A activity in insurance broking remained resilient throughout 2025, especially across continental Europe. Deal volumes continued at a solid pace, supported by a broad base of strategic buyers and financial investors with capital to deploy. In contrast, the UK market saw noticeably fewer announced transactions than in recent years, with deal counts down substantially compared with 2023 and 2024 as the domestic consolidation wave matured and available targets thinned.

Buyer behaviour also evolved. Acquisitions were increasingly targeted at strengthening specialty capabilities, building regional density and underpinning defined platform strategies rather than simply accelerating scale. Greater weight was placed on earnings durability, client retention and integration readiness, leading to more selective processes and clearer differentiation between assets.

Valuations and a more differentiated market

Valuation dynamics in 2025 became more nuanced and more closely tied to consolidation cycles and exit realities. Many private equity-backed platforms are now operating under second-round ownership, having entered at historically high multiples. As expectations around achievable exit pricing became more realistic, this discipline filtered through the market. Buyers became more cautious on bolt-on pricing, placing greater emphasis on earnings quality, integration risk and the credibility of post-transaction value creation, rather than paying up simply to sustain growth momentum.

As a result, valuation outcomes increasingly depended on how well a business was positioned and how broadly it was marketed. In a market with a diverse buyer universe, spanning strategic acquirers and financial sponsors at different stages of their investment cycle, creating the right competitive tension mattered more than ever. Clear positioning, credible equity stories and disciplined M&A advisory proved critical in translating underlying quality into strong valuation outcomes.

Integration, talent and execution risk

Another important lesson of 2025 was the renewed emphasis on integration as a core driver of value creation. Experience from recent transactions reinforced that scale alone does not deliver results unless systems, data and governance evolve alongside it. Several acquisitive groups deliberately moderated their deal pace during the year to focus on operating model consistency, technology integration and decision-making structures, recognising that complexity compounds quickly once platforms reach a certain size.

At the same time, AI emerged as a clear upcoming trend rather than a distant ambition. Broking firms increasingly explored the use of AI and advanced analytics to streamline placement processes, improve data quality, support client servicing and reduce administrative burden. While adoption is still uneven, the direction of travel is clear: firms that combine AI initiatives with strong data foundations and integrated workflows are better positioned to translate technology into practical productivity gains rather than isolated pilots.

Talent remains a structural challenge. Years of sustained M&A activity have contributed to experienced professionals leaving the sector, while regeneration from younger talent has been inconsistent. This has sharpened the focus on execution capability: the ability to integrate acquisitions, deploy new tools and consistently win new business ultimately depends on people. Not all platforms are equally prepared, and the gap between those that invest in talent, skills and culture and those that do not is becoming increasingly visible.

Carriers and MGAs reshape the ecosystem

Insurers and reinsurers also adjusted their approach during 2025. Even as pricing softened in some lines, underwriting discipline remained firm. Capacity was available, but increasingly allocated to distribution firms that could demonstrate strong risk selection, data quality and claims performance. Distribution relationships became more selective and more evidence-driven.

Alongside this, the managing general agent (MGA) market continued to move into the mainstream. Capital-light underwriting models, fronting solutions and specialist capacity gained further traction. MGAs increasingly play a central role in the distribution ecosystem.

Looking ahead

In hindsight, 2025 will be remembered as a year of recalibration for insurance broking. Growth did not disappear, but it became harder, more uneven and more dependent on execution quality. Consolidation remains a powerful force, but its success increasingly hinges on integration, talent and genuine commercial capability. As the sector moves into 2026, the message from 2025 is clear: scale still matters, but sustainable growth now demands far more than simply doing the next deal.

As the end of the year draws closer there was no real pickup in insurance distribution mergers and acquisitions (M&A) activity. With only a few weeks remaining in 2025, it is likely that the year will end with announced M&A volumes down by around a third relative to recent years. In value terms the drop is likely to be even more pronounced, as not only have there been fewer deals, but the average deal size has decreased. There have also been fewer very large deals announced in 2025. Taken together and barring the announcement of one or more mega-deals in the next 30 days, the value of sector deal activity in 2025 is likely to be the lowest since at least 2019.

M&A Market Update

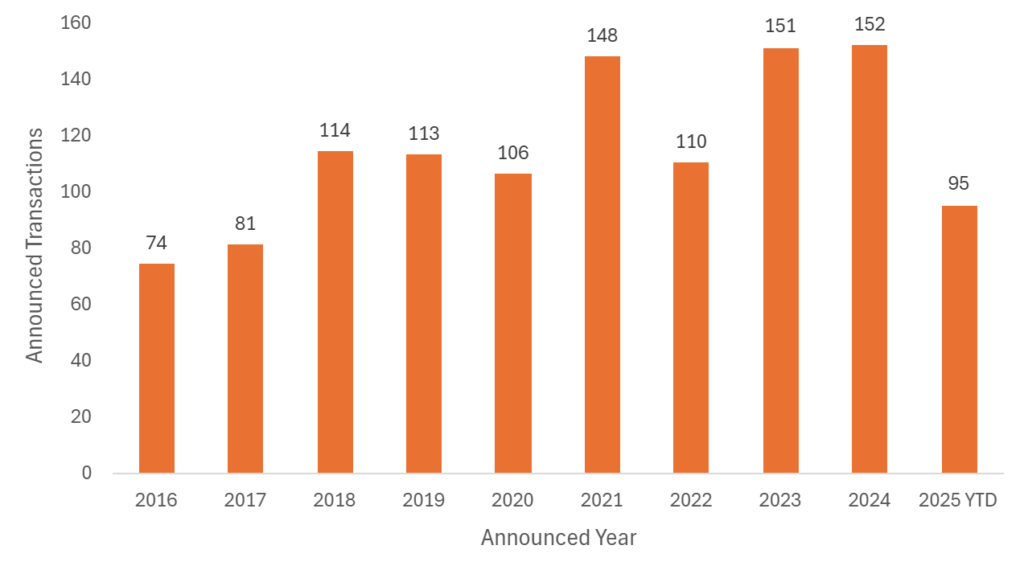

With eight new transactions to report on in November, the year-to-date (YTD) total stood at 95, against 144 at the same point in 2024, a decrease of 34%. December is a ‘short’ month in terms of business days and unlike the U.S. market it rarely results in a spike in UK M&A. There could be a slight uptick of new announcements in the coming days, as news of deals signed just prior to last month’s budget are made public. However, on the basis that Capital Gains Tax (CGT) was increased in 2024, and was one of few taxes where rumours had not been swirling in advance of Budget day, it is unlikely to be a major catalyst for transaction activity this year. Deal volumes for 2025 are likely to be above 100, as they have been in every year since 2017, but probably only just. MarshBerry will be publishing a detailed annual review analysing the full year in late February / early March. The 2024 review is still available to download here.

Total Volume of Announced UK Insurance Distribution M&A, Annual

Declining deal values remain a consistent theme

November’s new deals continued a theme that has run throughout 2025, in that they mainly involved smaller targets. Of the eight deals announced (and shown below) two were asset or ‘book’ deals rather than share acquisitions, only one involved a target employing ten or more staff, and the aggregate headcount across all deals in the month was only 54. Collectively they represent less than £10 million of income. Sector consolidation, measured by headcount and income, has slowed markedly in 2025.

MarshBerry will finalise the sums following the year end, but the combination of fewer deals, smaller deals, and a reduced number of very large transactions (there have been only five deals in 2025 with a value above £100 million), the overall value of sector M&A looks likely to be significantly lower than it has been for several years, and well below the c.£4bn it has averaged over each of the past three years. Of course, in any given year the total value of all sector deals tends to be dominated by only two or three ‘elephant’ transactions (think a GRP, CFC, PIB Group, or even JLT if one looks back a bit further) with a deal value that can exceed the combined total of the smallest 100 transactions in a year. (In 2024 there were 93 announced deals with an individual value estimated to be below £5 million.) There have been a handful of chunky transactions in 2025 (Jensten, Seventeen, BLP) but (so far) none substantial enough to get 2025 close to the level of any of the past five years.

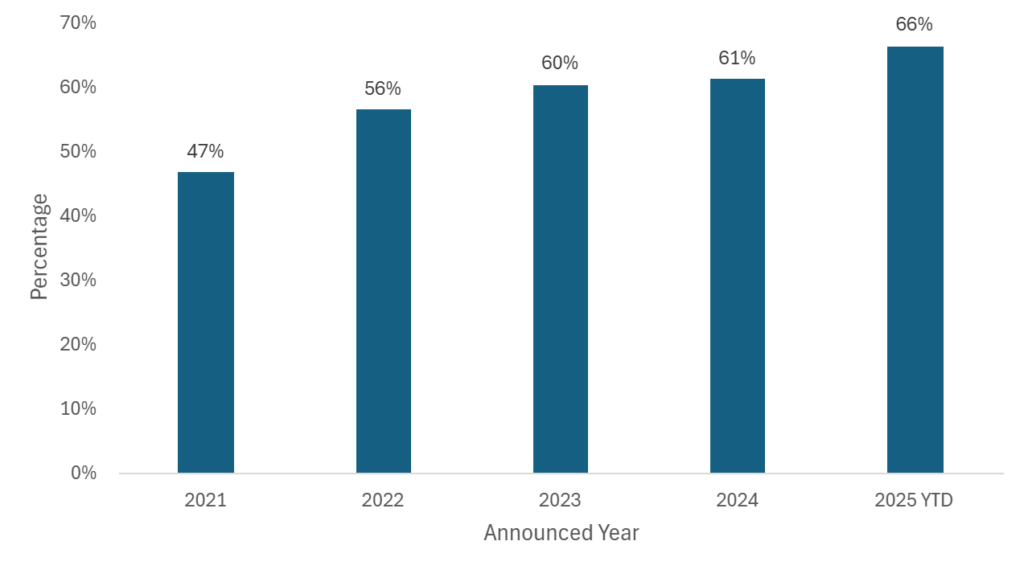

Of the 95 deals* YTD in 2025 MarshBerry estimates that 63 (or 66% of all deals) will have been done at a deal value of less than £5 million. This is a higher percentage than in any of the past five years, in spite of the impact of inflation and increased sector valuations over time, and above the long-term average (10 year) of 59% of all deals. Furthermore, only 13 deals in 2025 have involved targets with an estimated value of above £25 million.

The prevalence of smaller average deal sizes is likely to remain, because it reflects the remaining ‘supply’ of UK targets. Years of consolidation have hollowed out the number of privately-owned mid-sized brokers available to acquirers, but there are still a plentiful – albeit gradually diminishing – number of smaller (<10 staff) brokers left to go for. MarshBerry’s most recent analysis has the number of fully authorised groups at just under 2,000, or ~3,700 firms if including relevant Appointed Representatives.

Targets in UK M&A: Percentage of All Announced UK Deals Involving Target Valued Below £5m

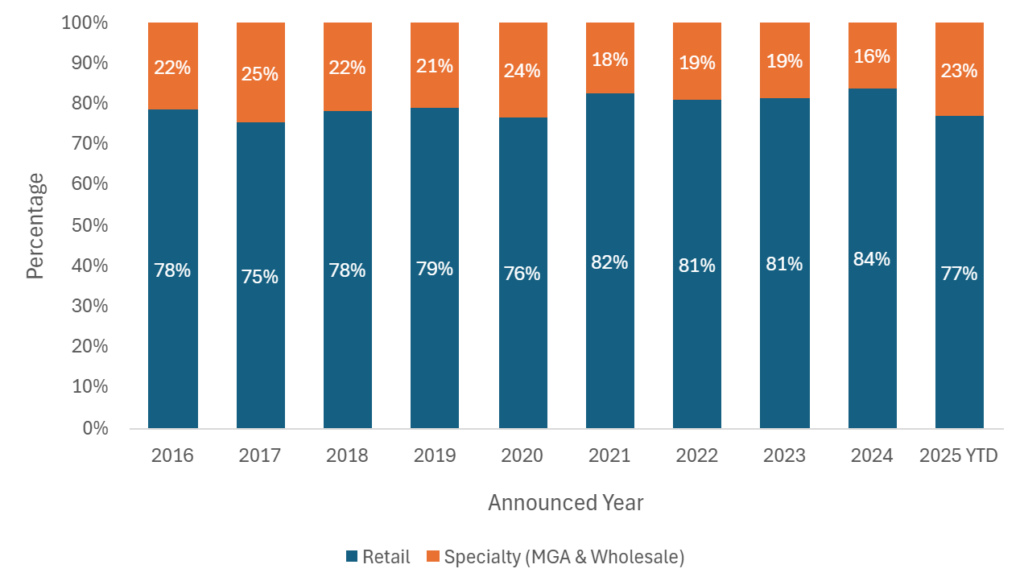

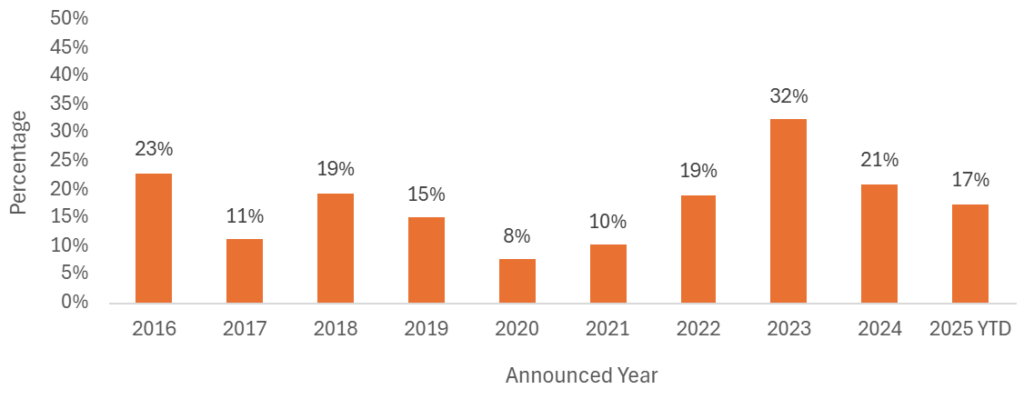

Specialty intermediaries continue to draw interest

One continuing bright spot in M&A activity in the UK has been in deals involving specialty targets, by which we mean wholesale brokers (including Lloyd’s Brokers) and Delegated Underwriting Authority Enterprises (read: MGAs or Managing General Agents), which borrows the U.S. terminology (MarshBerry defines specialty firms as those with delegated authority or that act as intermediaries between retail brokers and risk-taking markets).

Such firms are reportedly now forming at a faster rate than commercial brokers, typically have the potential to grow more rapidly on an organic basis (as wholesale business is less sticky), and are in high demand. Private equity (PE), overseas buyers, domestic consolidators of Lloyd’s brokers, MGAs and commercial business are all keen to acquire in the specialty segment. In 2025 YTD 23% of all deals have involved a specialty target, the highest proportion in the past five years, and there were two notable such acquisition in November (see below).

Targets in UK M&A: Retail vs. Specialty Distributors, % of Announced UK Transactions

Notable transactions (November 2025):

- In the latest example of a UK commercial lines focused broker acquiring a Lloyd’s broker, Partners& announced that it has acquired 3 Dimensional Insurance, based in Essex.

- PE-backed digital personal lines business Ripe announced the acquisition of Schofields, a long-established family-owned holiday homes specialist based in Bolton, adding a new arm and more than 10,000 policyholders to Ripe’s existing suite of leisure products.

- U.S. PE firm Aquiline (which also owns Ripe, above) announced a majority investment in Clearwater Underwriting, a marine MGA. Clearwater was only founded in 2024 and the investment highlights a growing trend of PE investors becoming involved in backing MGA businesses at a very early stage of their development, in order to support what can often be very rapid organic or inorganic growth.

Other transactions (November 2025):

- It was reported that Manchester-based motor broker Principal Insurance acquired the business of Peart Performance Marque, a personal lines broker that entered administration in October.

- Jensten Group, flush with new capital following its recent refinancing with Bain Capital, acquired Northern Counties, a commercial broker in the North East.

- Howden acquired the business of Church of Scotland Insurance Services, which provides cover for church properties through a scheme with Aviva, and with which Howden had an existing consultancy relationship.

- In addition to its 3DI deal noted above, Partners& added Avenue Insurance Partners, a trade credit specialist previously owned by the Tavistock Group.

- The Broker Investment Group (TBIG) owned firm Mark Richard Insurance acquired a controlling stake in Portal Broking Group in Cheshire.

* Note that the YTD figure of 95 includes two unannounced deals added to our listing during November but completed in July and August. These were identified via Companies House PSC notifications. This explains why the total in this Today’s Viewpoint increases by ten since the October publication, rather than the eight deals noted above.

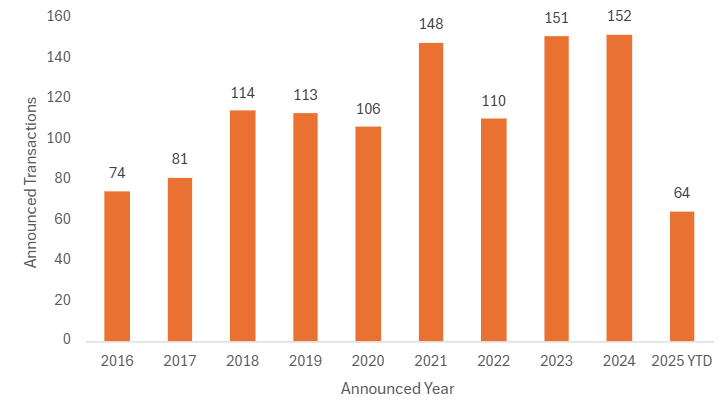

The fourth quarter got underway in October with another (relatively) busy month, with another ten transactions – the same number as last month – making it only the fourth month in 2025 where deal volumes reached double figures. Unlike in the U.S. market, where (for tax reasons) the last quarter of the year is always consistently more active than any other quarter, in the UK there is not really much seasonality in mergers and acquisitions (M&A). As such, with a year-to-date (YTD) total of 85 announced deals, it is clear that 2025 deal volumes will be materially lower than those in either 2023 or 2024, which both saw more than 150 deals in the sector.

M&A Market Update

October’s new deal count of ten was again marginally above the long-term average of 9.6 deals a month. There were 50 deals in the first half of 2025 and there were 35 in the first four months of H2 2025, in what has been a consistently slower year for sector M&A. At the same point in 2024 there were 126 announced deals, meaning this year has seen volumes drop by around a third.

Total Volume of Announced UK Insurance Distribution M&A, Annual

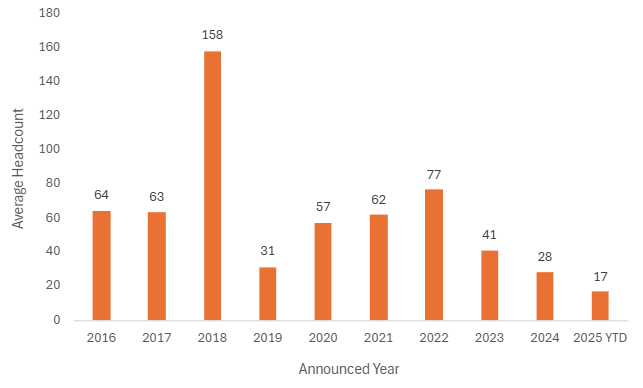

Demand remains but deal size is down

As MarshBerry has previously noted, 2025 has seen some of the most historically active buyers slow down their rate of acquisitions in the UK, including Ardonagh and Brown & Brown. There have been 47 separate buyers who made UK acquisitions in 2025, while ten separate firms have made two or more acquisitions. The top ten buyers have collectively been behind just over half of all M&A activity, so there is no shortage of demand. The most active buyer in 2025, by some margin, has been JMG Group. For the second successive month JMG Group announced a flurry of new deals (four in October, to add to their six in September) and as a buyer they represent more than 15% of all sector M&A volume in 2025.

But the number of deals does not tell the full story – to understand the real level of consolidation taking place it is important to look at the size of targets being acquired, and 2025 has seen a continued trend towards smaller average deal sizes. Average deal sizes are down again: in 2025 more than two thirds of sector M&A has involved a target with a value of less than £5m, against a long term (10-year) average of 59% of all M&A. This is before making any adjustments for inflation or increased sector valuations over the past decade and marks a continuing shift, as several mainly PE-backed consolidators get around the paucity of available mid-sized targets by doing mainly smaller deals in higher volumes.

Average Headcount of All UK M&A Targets (ex-Refinancing Deals) Acquired in Period

Note: 2018 jump is caused by inclusion of Jardine Lloyd Thompson Group (JLT)/Marsh deal. JLT had more than 10,000 staff.

This has certainly been true of JMG Group in 2025. Despite having done more than twice as many sector deals than the next most active buyer in 2025, its M&A activity involving broking and MGA targets has added just over 100 new employees, which in commercial business can be used as a broad proxy for income. Its average deal in 2025 has involved a target with fewer than ten employees. On a headcount basis, and excluding refinancing deals, it is actually only the third most active UK consolidator in 2025, marginally behind both NFP and Brown & Brown (Europe), whose deals in the year have both added more ‘heads.’

The trend towards smaller deal sizes also means that the continuing high (by historical standards) levels of deal activity are disguising the fact that in the absence of the occasional mega-deal, of which there have been none in the UK in 2025, the overall level of UK consolidation, as measured by GWP and income, has been falling. Given the continued demand for targets and ongoing, plentiful capital support for consolidation, this is clearly a supply-side driven reduction in activity.

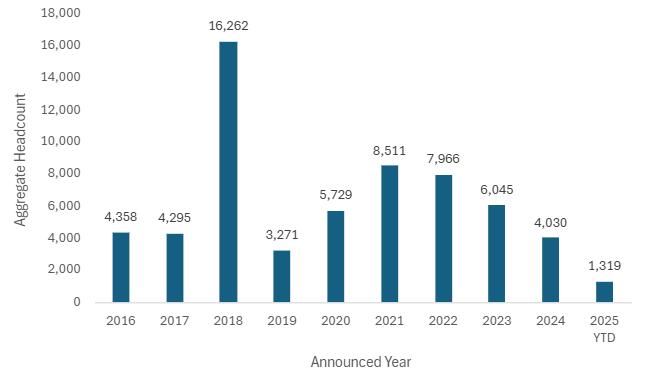

Aggregate Headcount Across All UK M&A Targets Acquired in Period (ex-Refinancing Deals)

Note: 2018 jump is caused by inclusion of Jardine Lloyd Thompson Group (JLT)/Marsh deal. JLT had more than 10,000 staff.

Private equity activity in the MGA segment

October also saw an exit by a private equity (PE) investor in the sector, with Beech Tree selling managing general agent (MGA) Avid to Bishop Street Underwriters, a U.S. consolidator that is itself PE-backed. This is the fifth exit for a PE-owned sector investment in 2025, and the second to a U.S.-based business. There have however been four new direct PE investments into the sector in 2025, broadly maintaining an equilibrium in terms of the overall number of PE-controlled UK insurance distribution groups, which has been gently edging down in recent years and currently stands at just below 40 – and of course includes some of the largest firms in the sector (Howden, Ardonagh, PIB Group).

PE interest in the sector remains strong and PE capital is still behind more than half of all sector deals in 2025. The MGA segment in particular continues to be closely evaluated by PE investors, who are attracted to its dynamism, potential for rapid growth, and perhaps encouraged by the sense that it has been less well pored over than commercial broking. This growing interest – and there’s likely to be more PE capital backing the MGA sector as it continues to grow and mature – comes notwithstanding the fact that in the UK PE investors to date have arguably had mixed results investing in MGAs (CFC being a very notable exception), which often have a very different risk profile to broking businesses and are by no means a “sure thing” from an investment perspective. There were three new MGA deals in October, and M&A involving MGAs has accounted for 17% of all deal activity in 2025, up from only 12% in 2024.

Notable transactions (October 2025):

- PE-backed MGA Avid Insurance announced its sale to Bishop Street Underwriters, the U.S. MGA consolidator that recently acquired Landmark Underwriting in the UK. Avid had been backed by Beech Tree Private Equity since 2019.

- JMG Group announced another four broking acquisitions in October, taking the firm’s deal count to ten in the past two months: Taveo Group in Scotland, Glowsure Insurance Brokers in Hampshire, James Brown & Sons in Somerset, and R Todd Insurance Services in Norfolk.

- Brown & Brown (Europe) added All Medical Professionals, which trades as All Med Pro Dental, a specialist broker based in Swindon and serving the dental, life science and hospital sectors.

Other transactions (October 2025):

- Howden announced two further UK deals in October, including Gott And Wynne, a commercial broker in North Wales that is best known for its classic car scheme for Morgan vehicles.

- In its second deal of the month Brown & Brown (Europe) also added Pardus Underwriting, an MGA based in Kent and focused on Property Owners and Commercial Combined business.

Today, top performing insurance brokers continue to be very attractive for acquisition by investors or strategic buyers. This appeal is not only due to favorable market conditions, but it’s also because these brokers deliver strong fundamentals, have recurring revenue and are remarkably stable during economic downturns.

The value of private equity (PE) investments in brokers reached a record high in 2024, with 2025 well underway to exceed this milestone. PE-backed buyers are now responsible for over 60% of all the deal activity in Europe.

A new class of investor-backed consolidators is rapidly emerging: financially strong companies that are attempting to triple their size within approximately five years using a ‘buy-and-build’ strategy. Their vision extends beyond their own market or region; consolidators think big, broad, and internationally. For independent brokers seeking growth or looking to map out their strategic options, a purely local perspective is no longer sufficient. They need to adopt an international vision. The critical question for independent brokers is whether they should follow the new market leaders or pursue alternative paths.

Insurance broking is no longer just local

The European insurance broker industry has long been defined by its local roots and fragmented structure, relying heavily on personal relationships and deep regional expertise. For years, small independent brokers held sway, offering customised solutions to meet the unique needs of their communities. However, this once localised and fragmented industry is undergoing a dramatic transformation.

The insurance broking industry has experienced a significant uptick in merger and acquisition (M&A) activity since the early 2000s, particularly in the U.S., where approximately 7,100 insurance brokers have been acquired in the past decade alone. This momentum quickly shifted to the UK, where the number of independent insurance brokers has nearly halved over the past 15 years. More recently, a growing number of buyers, many originating from the U.S. and UK, have shifted their focus to continental Europe, where consolidation efforts are steadily gaining momentum.

PE and PE-backed buyers have been a driving force behind insurance broker consolidation in Europe, and the record-high value of PE investments in insurance brokers was fueled by record-high levels of unspent cash reserves, commonly referred to as “dry powder,” much of which is still waiting to be invested.

MarshBerry reported 268 announced M&A transactions involving European insurance brokers in the first half of 2025 (through June 30). Private equity (PE) firms continued to deploy capital in insurance brokerage markets, while strategic buyers remained active, expanding their platforms across Europe through tuck-in acquisitions.

Why cross-border M&A is fueling European insurance broker consolidation

International acquirers (consolidators) are reshaping the sector, and they’re here to stay. An increasing number of European brokers are adopting buy-and-build strategies, not only within their own markets but increasingly looking across borders for attractive M&A targets. Just a decade ago, only the traditional Top 3—Marsh, Aon, and Willis—boasted a significant international presence across Europe. Today, scores of brokers are leveraging extensive networks of branches to operate across borders. It’s no coincidence that MarshBerry has published its first-ever Top 20 list of the largest European brokers this year. Ten years ago, such a list would have been meaningless; today, it clearly reflects that insurance distribution in Europe has become an international playing field.

Across European countries, a pattern is visible where national brokers are consolidating at all levels: from very small local books joining forces to top ten brokers merging. The result is a stream of domestic broker businesses, gradually scaling from small to mid-size to national champions and finally to European brokers. Targeting and acquiring insurance brokers in cross-border countries allows leading brokers to tap into new client bases.

These leading brokers have predominantly Anglo-Saxon origins and are mostly PE-backed. Among the Top 20 largest broker platforms in Europe, six have U.S. origins, while five are UK-based, reflecting the ongoing influence of these regions in shaping the European insurance broking market.

However, it is certainly not exclusively Anglo-Saxon brokers driving rapid market consolidation. Across continental Europe, new buy-and-build platforms are emerging at a fast pace. Traditional brokers acquired by PE undergo a complete strategic transformation, evolving into highly active players in the M&A market. For instance, in 2021, Germany’s oldest insurance broker brand, GGW Group (Gossler, Gobert & Wolters), transitioned with financing from Hg Capital and later Permira. Similarly, in 2023, the Dutch broker Licent Group secured funding from Gilde Equity Management, and just last year, the Belgian broker Induver merged with Clover with the support of Hg Capital.

Combining insurance broking and MGA power in Europe

Consolidators in the European insurance distribution market are increasingly combining traditional insurance broking with MGA (Managing General Agent) capabilities to boost margins and create more competitive platforms. By integrating MGA expertise, these firms can underwrite niche or specialty risks, offer tailored products, and capture a larger share of the margin within the insurance value chain. This hybrid model not only enhances revenue streams and operational efficiency but also strengthens the ability to serve diverse client needs across multiple markets.

The landscape for MGAs in continental Europe is varied and diverse:

- Germany has had a robust MGA market for many years, with a wide range of MGAs operating across niche segments and a concentration in marine.

- France, Italy, and Spain are all experiencing a growing MGA sector, particularly in niche insurance products for both commercial and personal lines.

- The broker landscape in the Netherlands is distinctive, with many large retail broker firms operating their own MGAs.

- The Nordic countries, including Sweden, Denmark, Norway, and Finland, have a strong presence of MGAs focusing on marine, renewable energy, and other specialised insurance sectors.

The total number of sizeable MGAs in continental Europe is estimated by MarshBerry to be around 500. However, this figure is approximate, as most European countries do not track the number or activities of MGAs.

The strategic reality facing independent brokers

Europe still has a large number of independent insurance brokers. According to MarshBerry’s analysis, there are over 100,000, ranging from many small firms—often sole proprietorships—to mid-market firms and large enterprises. The management teams and owners of these independent brokers need to recognise that the market is changing. The era of insurance broking as a purely local business is over. International market leaders are set to grow even larger in the coming years, while new entrants, backed by private equity, will continue to pursue buy-and-build strategies.

So, what is the bottom line for independent insurance brokers? They must decide how to respond. Entrepreneurs in this sector cannot afford to ignore the profound transformation underway. Ignoring change ultimately means you won’t survive.

Transferring your company to a strong external buyer can be a smart decision, aligned with your company’s lifecycle. But following the market leaders is by no means the only option. Every insurance broker with strong performance, solid organic growth, and good profitability should recognise that numerous strategic opportunities exist.

In today’s market, it is a matter of putting all options on the table: pursuing independent organic growth, attracting an investor, selling your firm to a strategic buyer, or joining forces with other brokers to form a new broker group. Now is the time to assess your strategic options and prepare for what lies ahead.

The third quarter came to an end with a flurry of new deals being announced, with September’s ten transactions making it the busiest month since April 2025 (which was of course the end of the last tax year). The quarter ended with 25 transactions, down from the 30 in Q2 and bringing the year-to-date (YTD) total to 75 deals. At the same point in 2024 the total transaction count was 114, meaning deal volumes are running 34% below the prior year. September also saw one of the biggest deals of the year – the widely trailed refinancing of Jensten Group – and a number of much smaller ones. JMG Group, with six new acquisitions announced this month, has set a recent buyer record for the most deals in a single month.

M&A Market Update

September’s new deal count of ten was (just) above the long-term average of 9.6 deals a month and began with one of the biggest deals of the year: private equity (PE) investor Bain Capital acquiring Jensten Group from Livingbridge, which first backed the business (which was then still called Coversure) in 2018. With around 1,000 staff, Jensten is the largest UK insurance distribution business (based on headcount) to have sold in 2025. Bain Capital is no stranger to the sector and earlier this year made a major investment in U.S. broker Acrisure, which has also been acquisitive in the UK but has recently slowed down M&A (mergers and acquisitions) as it seeks to deleverage, ahead of a planned IPO expected in 2026. With the new backing, Jensten is expected to again become more active in UK M&A, where it had slowed down its pace of acquisitions over the past twelve months (although it has still been quietly working on some deals and acquired a small commercial broker in Kent in August).

Total Volume of Announced UK Insurance Distribution M&A, Annual

Private equity buyers maintain pace

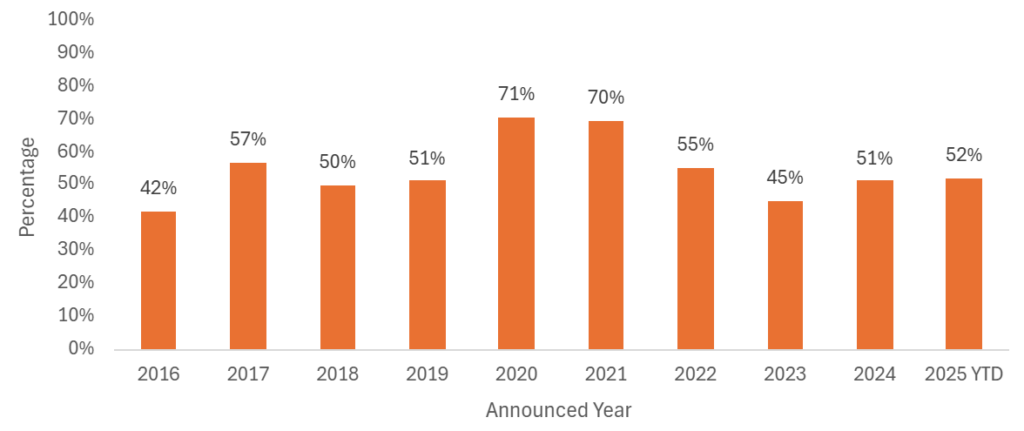

A running theme in 2025 had been a modest reduction in the proportion of UK M&A transactions that involved PE, either directly or indirectly (i.e., where the acquisition was made by a PE-backed firm). However, nine of the ten new deals (which incidentally all involved commercial broking targets) in September involved PE and given the relatively low volume of deals overall in 2025, this has pushed the proportion to just above half of all deals, which is consistent with 2024. Bain’s investment in Jensten Group is the fourth £100m+ UK transaction of 2025 involving a PE buyer, demonstrating that the consolidation opportunity in the sector still holds appeal and is attracting PE capital, even as deal volumes have fallen and the underlying pace of consolidation has slowed.

Private Equity-Backed Transactions as % of Total, Announced UK Transactions

JMG Group, with fresh backing from GTCR, announced six new deals in September. There is of course bound to be a “London buses” effect (younger readers who have grown up knowing only digital bus stop displays may have to Google what this means …) in this number, with deals that have been worked on over the summer and granted regulatory approval by the FCA all completing around the same time and being announced together. Nevertheless, six deals in a single month is no mean feat and demonstrates that the business is able to successfully identify, negotiate and perform due diligence on a large number of deals in parallel. The six businesses acquired were all relatively small and in aggregate, add fewer than 30 employees to the group, which is less than most medium-sized firms. However, medium-sized firms are now in short supply, and generally cost buyers more than small firms (<10 staff) where unadvised deals are routinely done at single-digit multiples of EBITDA. For buyers that can do these deals in consistent volumes, and then integrate the targets effectively, improving their operating margin along the way, they can be highly accretive to value.

Overseas buyers deal volume declines, but interest remains

UK M&A: % of Announced UK Transactions involving an overseas buyer

Other buyers in September included Partners& and Specialist Risk Group, both UK firms. There have been 45 unique buyers in 2025, across 75 deals. Only 13 transactions (or 17% of all deals) have involved an overseas buyer, which is the lowest level since 2021. However, this does not mean that the UK has lost its allure for overseas acquirers, or that the trend of increased internationalisation and cross-border M&A has reversed. It is largely the result of a reduced volume of smaller UK M&A from some of the U.S.-based acquirers that have been most active in recent years (e.g., Gallagher, Brown & Brown) during a period when several domestic UK consolidators have been very busy (e.g., the aforementioned JMG Group).

Those same U.S. buyers have been undertaking large transactions over the past twelve months, including in overseas markets. More North American buyers continue to weigh up acquisitions in the UK and there’s likely to be continuing inflows of U.S. (and indeed European) capital into the sector in the coming months.

Notable transactions (September 2025):

- The biggest transaction of the month saw U.S. PE firm Bain Capital acquire consolidator Jensten Group from Livingbridge, in a deal that had been widely expected following reports in the trade press several weeks ago. It was widely known that Livingbridge had been seeking an exit.

- JMG Group announced six acquisitions: Allsop Commercial Services in Gainsborough, Highhouse Insurance Services in Sussex, Insursec Risk Management in Essex, Boston Insurance Brokers in Solihull, Hayton Insurance Brokers in Kendal, and Gateway Insurance Services in Scotland.

- Specialist Risk Group continued its strong run of deals in 2025 with the acquisition of Champion Insurance Group, a retail broker based in Manchester that will strengthen SRG’s presence in the North West.

Other transactions (September 2025):

- Partners& acquired Citytypes, a commercial broker in Nottingham that trades as Pargeter & Associates.

- In August Jensten Group acquired Martin Insurance Services in Kent. Note, this deal was not reported in MarshBerry’s August UK M&A Update but is being included here and is in the figures above. During September Lloyd & Whyte was reported in the trade press to have acquired holiday home specialist Boshers, in a transaction that was highlighted in their annual report but had in fact happened several months ago.

It may have been a warm August, but for buyers and sellers in UK insurance distribution mergers and acquisitions (M&A) it was an uncharacteristically cool month, with only five new sector deals to report on. It is now two thirds of the way through 2025 and there have only been 64 announced transactions during the year. To put that in context, by the end of August in both 2023 and 2024 there had been more than 100 deals announced. On a year-to-date (YTD) basis M&A volumes are down 38% on 2024 and at the current run rate, 2025 is shaping up to be the quietest year for deal activity since 2017. But deal statistics in isolation are pretty uninteresting – the important questions are really around why this has happened in 2025, and when, why and whether this trend might reverse.

M&A market update

With only five new deals during the month, it was the quietest August for UK insurance distribution M&A since 2016 and well below the long-term UK average of 9.6 deals a month. But the month did see one sizeable deal announced, with the news that Leeds-based MGA platform Bspoke Insurance has been acquired by NFP, itself now part of Aon. With Aon now clearly acquisitive in the UK again (they acquired Griffiths & Armour in 2024) after several years focused solely on organic growth here, there is some speculation that either Marsh or Willis may similarly begin to look more closely at UK acquisitions.

Total Volume of Announced UK Insurance Distribution M&A, Annual

Demand and supply

So what is behind the lull in deal activity in 2025? As always, there is no simple explanation and no single factor at play. MarshBerry UK has discussed at length that after years of consolidation there is a reduced supply of suitably attractive brokers available for acquisition by the consolidators, particularly at the medium-sized level (20+ staff) that can really move the needle. But this was equally true in 2024, when M&A volumes were running at record levels. So it is not just a supply issue. Does looking at the demand side yields more answers?

Rates have softened in 2025. This has put pressure on broker revenues and EBITDA (earnings before interest, taxes, depreciation, and amortization). No one can say with any real certainty when this situation will reverse. Interest rates (i.e., debt costs) remain above the longer-term average and wider macroeconomic uncertainty remains high. Inflation and higher staff costs are squeezing margins in many businesses.

These uncertainties have made capital providers – including (crucially) the private equity (PE) investors that have fuelled so much sector M&A – more skittish. Additionally, big sector deals and refinancings closing at lower-than-expected multiples have made them nervous about their own exit value assumptions, which in turn colours their views on the acquisitions their portfolio companies are making. Depressed M&A valuations for unintegrated groups have also undermined the idea that size alone should command a premium – coherence matters, which is increasing buyers’ selectivity and putting more emphasis on integration. The big deals, both the ones that happen and the ones that don’t, are also a major distraction for management, acting as a further brake on smaller ticket sector M&A.

A shifting backdrop for valuations

Against this backdrop, deal valuations have eased back from multi-year highs. This in itself can derail or prolong transactions. Vendors are (unsurprisingly) quick to adapt and adjust their expectations when prices are rising, but they are somewhat less biddable when the opposite occurs. It can be difficult to psychologically accept that your business, which might be trading very well and still growing, is worth less to a buyer than it was six months ago. A gap between the prevailing views of buyers and sellers on value has prolonged, postponed or indeed killed off several deals in 2025.

What next?

Will the situation reverse? And when? While no one can point to a single event or catalyst that will drive deal activity up again, insurance distribution’s robust fundamentals are unchanged, including: Products that will always be required, high levels of renewable income, cash generation, low capital requirements, opportunities to improve efficiency and grow margins through better use of technology, and a (still) high level of fragmentation, with many hundreds of privately owned UK firms in the hands of ageing individuals that will in most cases elect to sell to a larger firm. Sector consolidation will not stop and PE appetite for the segment will not disappear, while the drivers of both continued domestic consolidation and increasing cross-border M&A will remain in place.

And as for those uninteresting deals statistics, see below. PE and PE-backed transactions have accounted for 45% of sector deals YTD and are running at the lowest level for several years. Specialty targets (being MGA and wholesale business, including Lloyd’s brokers) have accounted for more than a quarter of all deals in 2025 (and three of the five deals in August), above the longer-term average, and are seeing continued robust demand from both dedicated consolidators, groups seeking to widen their existing capability, and overseas buyers.

Private Equity-Backed Transactions as % of Total, Announced UK Transactions

Source: MarshBerry Proprietary Database and Companies House. Data as of 8/31/2025.

Targets in UK M&A: Retail vs. Specialty Distributors, % of Announced UK Transactions

Notable transactions (August 2025):

- The biggest transaction of the month saw MGA platform Bspoke Insurance being acquired by NFP, which is now part of Aon. Bspoke had been backed by PE (RCapital) and so the transaction is another example of PE capital flowing out of the sector and a further concentration of sector ownership in the hands of the large U.S.-listed multinationals.

- Specialist Risk Group continued its strong run of deals in 2025, during which it has acquired both in the UK and overseas, with the acquisition of City Quarter Brokers, a London-based wholesale broker with a global footprint and focused on the construction, engineering and infrastructure sectors. MarshBerry advised City Quarter Brokers on the transaction.

- Liberty Blume, the business solutions arm of multinational Liberty Global and whose activities also include providing working capital solutions for corporate clients, announced the acquisition of PHL Insurance Brokers, a small Lloyd’s broker. The deal is something of a collector’s item for sector M&A watchers, being a rare example of a strategic buyer from outside the industry getting into broking through the acquisition of a regulated business and again demonstrating that the right buyer of a business can sometimes come from leftfield.

Other transactions (August 2025*):

- It was reported during the month that David Roberts & Partners, itself part of BMS, acquired London-based Umbrella Insurance Services.

- In its fifth announced acquisition of 2025, Peter Cullum’s The Broker Investment Group announced the acquisition of KSL Thomas Insurance, a £2m GWP commercial broker in Essex.

* Eagle-eyed readers may be wondering why JMG Group’s acquisition of PI MGA XS Assure is not included here, having hit the headlines during August. The deal was actually completed in July and identified and included in MarshBerry’s July Viewpoint figures, albeit without MarshBerry actually naming XS Assure.