The UK wealth management sector is undergoing a decisive structural shift. While merger and acquisition (M&A) activity remains robust across the market, it is increasingly concentrated among large, private equity (PE)-backed consolidators – and the performance gap between scaled businesses and smaller, owner-managed firms continues to widen. Scale is no longer just an advantage; it is becoming the currency of value creation in wealth management M&A. This dynamic is reshaping outcomes for both acquirers seeking sustainable growth and sellers assessing the long-term value of independence.

M&A is flowing toward scalable business models

Nearly half of all UK investment sector transactions in 2025 occurred among asset managers and integrated wealth managers, businesses that combine financial planning with discretionary portfolio management. These firms are attractive not simply because of their size, but because their operating models are repeatable, scalable, and commercially proven.

At the same time, advisory-only firms, particularly smaller independent financial advisors (IFAs), continued to see declining share of deal volumes and aggregate transaction values. While these businesses remain economically relevant, buyers are becoming more selective, prioritising targets that can either accelerate platform growth or be efficiently absorbed into existing infrastructure. This explains why PE-backed consolidators accounted for more than a quarter of all acquisitions, completing multiple deals every year. The result is a market where size attracts capital and capital enables further size.

Scale drives faster revenue growth – and it’s compounding

One of the most striking outcomes of the past year is the clear correlation between firm size and revenue growth. Among wealth management businesses filing full accounts, the top revenue quintile achieved a 16% compound annual growth rate (CAGR) over three years, while the bottom quintile recorded effectively zero growth over the same period. This divergence reflects more than acquisition activity alone. Larger firms benefit from dedicated growth teams and professional management, access to capital for both organic investment and M&A, and the ability to cross-sell broader propositions to existing clients.

Smaller, owner-managed businesses often lack the financial or managerial capacity to pursue these strategies at scale, limiting both growth velocity and optionality. Over time, this gap compounds, making it increasingly difficult for subscale firms to “catch up” organically.

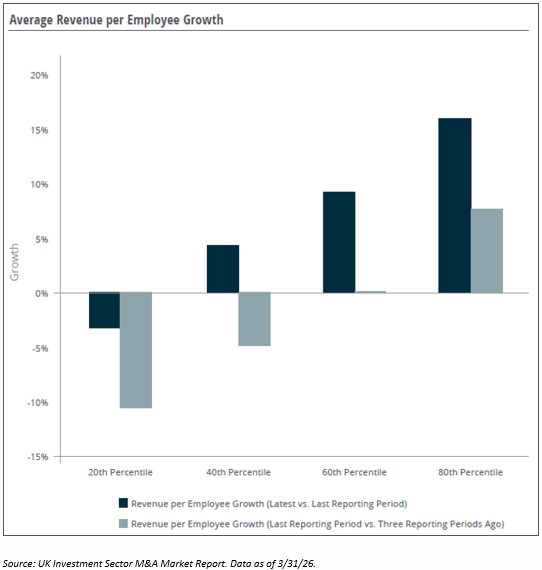

Productivity is the operational proof point

Revenue growth alone does not explain the valuation premium achieved by scaled firms. Productivity – measured as revenue per employee – provides the operational proof of scalability.

Revenue per employee growth is strongly correlated with firm size. The chart below illustrates the widening performance gap in UK wealth management. Larger firms are delivering materially higher revenue growth per head than smaller peers, reflecting the advantages of scale as described above. As consolidation continues, scale remains a defining driver of growth and long-term value creation.

Larger acquirers are realising efficiency benefits from centralised compliance, admin, and technology plus standardised investment propositions and broader client wallet penetration. For buyers, this reinforces that productivity delivers the ability to support further acquisitions while for sellers, it increasingly defines how attractive their businesses truly are.

Valuations reward scale, predictability and momentum

While average valuation multiples in private wealth transactions remained broadly stable in 2025, there were fewer deals at extreme highs or lows with more deals priced close to the average multiple, suggesting buyers are pricing risk more consistently. Crucially, firms that combine consistent revenue growth, strong revenue per employee metrics, and clear post-transaction integration potential continue to command premium outcomes.

This helps explain why larger, diversified wealth managers traded at higher earnings multiples throughout 2025, supported by earnings growth and more resilient outlooks than the broader market.

In contrast, smaller firms face increasing valuation pressure as buyers discount execution risk and future scalability.

Fragmentation keeps the consolidation engine running

Despite years of dealmaking, the UK IFA market remains highly fragmented, with:

- Over 6,000 wealth management entities operating nationally.

- 91% of firms still privately owned.

- Nearly 90% of analysed businesses employing fewer than 50 staff.

This fragmentation ensures that consolidation pressure will remain high. But the nature of consolidation is evolving as recent activity shows fewer, larger transactions, greater competition for quality targets, and rising expectations around integration readiness and cultural alignment. In this environment, scale is becoming both a defensive shield and an offensive weapon.

Implications for buyers and sellers

For acquirers, the data reinforces that M&A success is no longer about volume alone. Platforms that can integrate well, protect productivity, and compound growth are best positioned to raise capital and sustain valuation premiums.

For sellers, the gap between being acquired as a “strategic platform” versus a “bolt-on” is widening. Building scale, either independently or through earlier partnerships, can materially influence not just if you exit, but how you exit.

The 2025 data confirms what the most active participants already know: scale is no longer just a growth lever – it is a determinant of relevance, resilience, and value in wealth management M&A.

As consolidation continues, the market will increasingly reward firms that have invested early in people, infrastructure, and repeatable growth models. Others will be forced to decide whether independence remains viable or whether scale now requires partnership.

Get the full picture

For the latest data, M&A trends, and in-depth analysis of the UK wealth management sector, download the exclusive MarshBerry Investment Sector M&A Market Report.