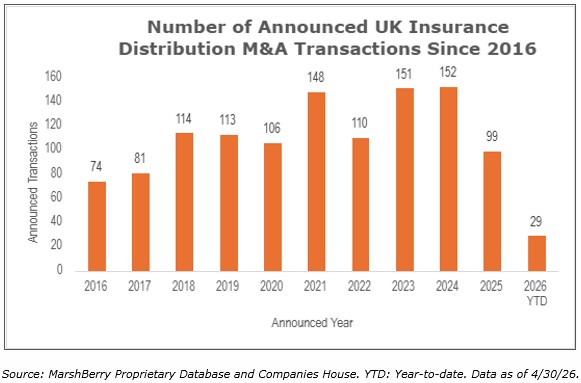

Mergers and acquisitions (M&A) deal activity in 2026 has so far remained depressed, as it was throughout 2025, which is inevitably raising the question of whether this is a temporary response to broader pressures in the sector or a ‘new normal’ for a market approaching the later stages of consolidation. On a year-to-date (YTD) basis there have been only 29 announced deals in the UK. At the same point in 2025 – which was itself the slowest year for sector M&A since 2017 – there had been 37. That said, April saw nine new deals announced, the highest monthly total of the year so far, including a number of relatively sizeable and high-profile transactions.

M&A Market Update

With nine new deals, including two involving targets employing more than 100 staff, April was the busiest month of 2026 so far and the most active for sector M&A since last October. It also marked the beginning of a new tax year, and with it a modest increase in the amount of tax incurred by private sellers on a sale of their business. The rate of Business Asset Disposal Relief (BADR) has increased from 14% to 18%. On the basis that BADR is available on proceeds up to £1 million, the impact of this is up to £40,000 for every eligible seller, so relatively modest in the context of most sector deals. It was evidently not enough to precipitate a rush of M&A before the deadline, but of course the planned increase has been known about for 18 months and so any sellers driven by concern around this have had plenty of time to act. Contrast this with last April, which was comfortably the most active month of 2025 for M&A with 17 deals. BADR at that time increased from 10% to 14% – so the same amount, but in a change that had only been announced six months beforehand (in the October 2024 budget).

That monthly difference has impacted the year-on-year (YoY) comparables. Year-to-date the deal count for 2026 is at 29, compared to 37 at the same point in 2025, a 22% reduction against what was a very slow year for deals. On a run rate basis it looks as though the market may again be looking at an annual deal count of below 100. The nine deals in April 2026 are still below the ten-year average of 9.6 deals per month.

A return to bigger deals?

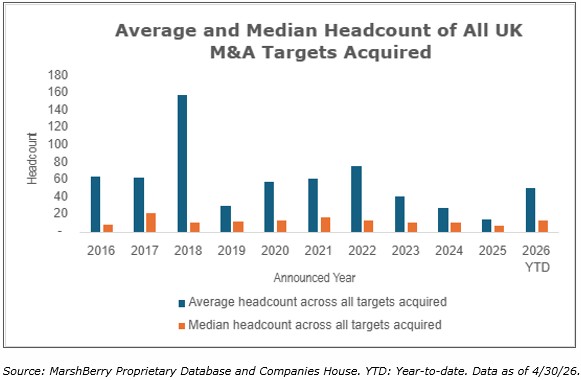

Of course, deal volumes are not the whole story. The size of those deals matter. To understand the real level of sector consolidation, in terms of GWP and income, it is important to analyze the firms being acquired. MarshBerry tracks the reported headcount of every deal in the sector, which can be used as a proxy for income. Average sector deal sizes have been falling, and the aggregate headcount ‘acquired’ through M&A has been steadily decreasing for the past five years.

On this metric, 2026 is not shaping up to be as quiet as it might first appear, and the new deals announced in April are part of that story. Bridge Insurance Brokers, Eaton Gate and U Drive Cover (see below) were all sizeable transactions. The average headcount across announced deals in the month was 46. Year-to-date it is 53. The nine deals in April involved targets collectively employing more than 400 staff and YTD sector M&A has involved targets with an aggregate headcount of more than 1,500.

In 2025, ignoring refinancing deals (i.e., not real consolidation), fewer than 1,400 ‘heads’ were consolidated. Granted, one large deal (the acquisition of Prestige by AUB) accounts for a large chunk of the total in 2026, but the numbers point to 2026 seeing a greater level of overall industry consolidation than last year and demonstrate that in spite of a slowdown in transaction volumes, bigger deals are still getting done.

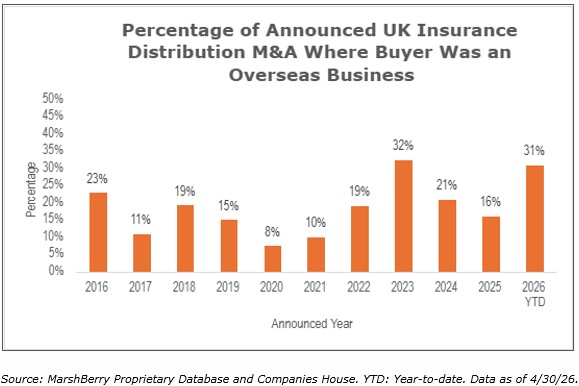

The real ‘special relationship’?

April’s deals also demonstrated that overseas buyers remain highly relevant and active in the UK. Four of the nine new deals during the month involved a U.S. buyer. Nine of the 29 deals (31%) in 2026 YTD have involved an overseas buyer, with all but one of those buyers coming from the U.S. And with DOXA’s acquisition of Eaton Gate, the market has a further new entrant.

“New new” buyers (i.e., acquirers entering the market for the first time) to the UK are actually relatively rare. There have been fewer than 25 over the past ten years. Most U.S. buyers in the UK have been here for many years (think Gallagher, Acrisure). DOXA has indicated that it wishes to do more M&A here, and there are several other specialty platforms (MGA (managing general agent) and wholesale) from the U.S. actively exploring deals here. U.S. capital targeting UK specialty targets in particular is a trend that will likely continue in 2026.

Explaining the drop in deal count – supply and demand

Many of the most active broking consolidators have become more cautious around M&A in recent months. Integration of past acquisitions has become a higher priority, reflecting the higher valuations that the market is now demonstrably ascribing to the most cohesive and operationally disciplined groups (or, conversely the discount being applied to the more fractured and fragmented consolidators, if you wish to look at it the other way round). Across several previously very active buyers there is an ongoing shift in focus away from the high-volume approach to M&A that has characterised the past few years. MarshBerry will be publishing a separate piece on this topic very soon, and covers it in further depth in the recent The State of the UK Insurance Distribution market report, available here.

This slowdown is a demand-side factor, but of course there is absolutely no shortage of demand for quality broking and MGA targets in the UK. Indeed, £ millions of new private equity money has entered the market over the past 18 months. The more pressing constraint is on the supply side. There just aren’t enough available targets of meaningful scale and quality to go around. The report noted above sets out exactly how many.

Notable transactions (April 2026):

- Arthur Gallagher announced the acquisition of Bridge Insurance Brokers in Manchester. Bridge is particularly well known for its expertise in property and construction and is one of the largest remaining independent brokers in the UK, employing more than 100 staff.

- In its largest acquisition to date, adding £38m in GWP, The Broker Investment Group announced a deal to acquire a 75% stake in U Drive Cover, a motor broker focused on more complex risks. The transaction is only the third deal in 2026 involving a personal lines business.

- Continuing the recent trend of cross-border transactions involving specialty targets, MGU Eaton Gate announced it has been acquired by DOXA, a PE-backed consolidator of MGA businesses that has been active in the U.S. but is a new entrant to the UK. DOXA has indicated that Eaton Gate will be used as a platform for further acquisitions in the UK and Europe.

Other transactions (April 2026):

- U.S. consolidator Acrisure added to its UK business with two new acquisitions,* announcing deals for net worth broker Smith Greenfield Services, which also includes the Confidas trading stye (used for its MGA business) and Heathwoods Insurance & Financial Services, a broker focused on the property and construction sectors.

- Clear Group continued in its consistent run of M&A with two new commercial broking acquisitions, adding Pangea Insurance Brokers in Hampshire and Spence (Insurance Services) in West Lothian.

- Partners& announced the acquisition of Barnett & Merriman (which trades as Amica Insurance Brokers), a broker in Staffordshire.

- Seventeen Group announced a deal for 1st Choice Insurance, a specialist fleet broker with a reported £13m of GWP and based in Shropshire.