M&A Market Update

Following the trend from last year, private equity (PE) funds continued their active engagement in the sector in seven of the eight deals during January. It included yet another sizeable wealth manager, The Private Office, attracting capital and adding to the growing number of PE-backed vehicles in the UK wealth management space. There were five announced add-on purchases between four firms – Verso Group, W1M Wealth Management, Wren Sterling and Titan Wealth.

The sector also saw PE interest in the business services segment of the market with Pollen Street Capital acquiring the fund services platform Tutman (Thesis Holdings Limited). Also in line with last year’s developments, EQT’s acquisition of Coller Capital, one of the world’s largest secondaries managers, was an example of the strategic interest in managers of alternative assets. It is another indication of how leading UK businesses in the sector are attracting attention from international acquirers.

Total Announced UK Investment Sector Transactions, Annual

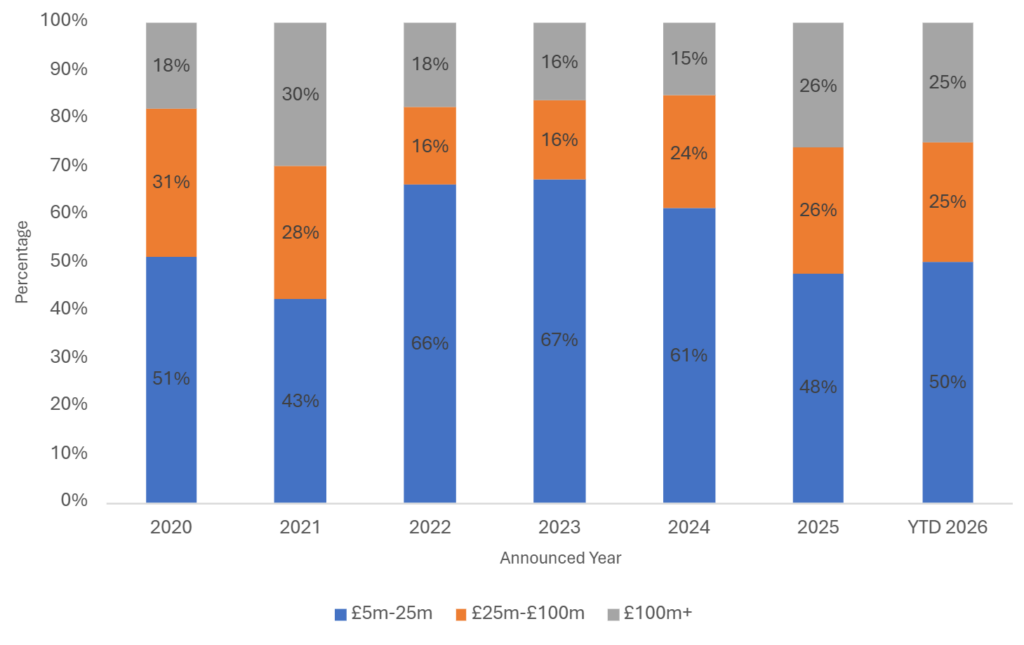

Deal values in January covered a broad range with similar distribution to last year, with two deals above £100m, two in the mid-sized bracket (£25m-100m) and the balance being smaller transactions. At $3.7bn maximum consideration, EQT’s acquisition of Coller Capital was significant, marking a strong start to 2026. 2025 resulted in a record year for the aggregate value of deals above £5m and showed increasing deal count in the large and mid-sized segments where businesses are targeted by a growing number of larger consolidators and strategic acquirers. January provides support for that trend to continue this year, especially in the mid market with its higher density of available targets.

Announced UK Investment Sector Transactions by Target Size

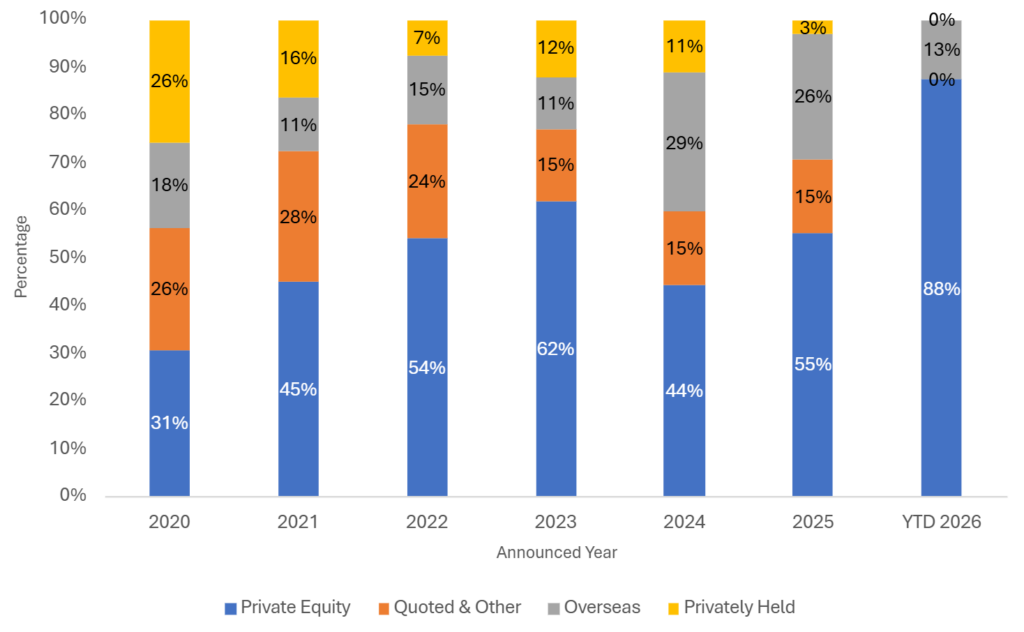

Private equity was the most dominant acquirer type during January, investing either directly or indirectly via their portfolio companies. All deals in January featured a PE buyer – in some form. One of the eight deals was transacted by an overseas PE firm acquiring capabilities for its own operations (rather than investment on behalf of a fund).

The growing number of businesses being backed by PE funds will have a profound impact on developments in the sector and be a strong force for change of structure, growth and prospects.

PE-Backed Transactions as a % of Total Announced Transactions

Notable transactions (January 2026):

- EQT announced the acquisition of global secondaries firm Coller Capital. Coller provides liquidity solutions to both general partners and limited partners, investing across private equity secondaries and private credit secondaries. The acquisition enhances EQT’s ambition to develop a private markets firm of scale, adding Coller’s team of 330 professionals, 11 global offices and nearly $50bn of assets under management (AUM).

- Pollen Street Capital announced it had acquired Thesis Holdings Limited (Tutman). Tutman is a fund services platform providing fund administration, corporate service and transfer agency services to institutional investors, wealth managers and family offices. The acquisition represents an opportunity for Pollen Street to develop a scaled, fund services platform and continues its strategy of backing specialist financial services platforms.

- The Private Office (TPO) announced it had received a minority investment from Goldman Sachs Alternatives. Leeds-based TPO is a chartered independent financial advice and planning firm with a nationwide presence, 181 staff and £3bn of client assets. Goldman Sachs Alternatives will support TPO through its next phase of growth.

Other UK transactions (January 2026):

- W1M Wealth Management announced it had acquired independent wealth and investment management firm Vermeer Partners. Vermeer has £2bn in AUM and marks W1M’s first acquisition since Waverton and London & Capital merged in July 2024.

- Titan Wealth announced the acquisition of two financial advice firms: Chester-based Innes Reid Investments (£590m of assets under advice (AUA)) and Plymouth-based Sound Financial Management (£600m of AUA).

- Verso Group announced the acquisition of Midlands-based chartered financial planning firm Everlong Wealth, adding over £350m of client assets.

- Wren Sterling announced it had acquired Gloucester-based advice firm Brunsdon Financial, adding 800 households and £265m of AUA.

- Cooper Parry Wealth announced the acquisition of Wimbledon-based independent chartered financial planning firm Gem & Co.