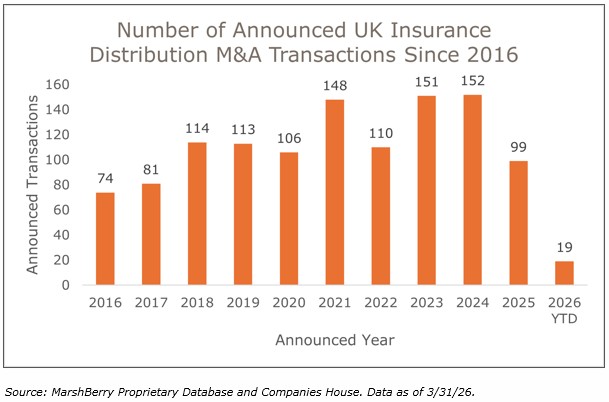

Despite a handful of interesting and relatively sizeable transactions announced in 2026, March was yet another slow month for insurance distribution mergers and acquisitions (M&A), with Q1 2026 being the quietest quarter for deal activity in over five years. It was the slowest quarter since Q2 2020 (remember what was happening then?) and there have been only six quarters over the past ten years where there were fewer deals. Deal activity looks unlikely to bounce back to 2023/24 levels in the near future, with 2026 already shaping up to be another muted year for sector M&A volumes, just as 2025 was.

M&A Market Update

There were 19 M&A transactions announced in Q1 2026, one less than at the same point last year and substantially below the longer-term quarterly average (28.5). It is a long way behind the busiest quarter for deal activity (Q1 2021) when there were no fewer than 55 new deals announced. At the current run rate, 2026 is looking like it may be another year where deal volume will come in below or around 100, as they did in 2025, and well below the levels of the most frenzied recent years.

In reading this you will no doubt be feeling sorry for the author of this piece, having to find something interesting to write about every month against such a backdrop, but do save some sympathy for the beleaguered (and expensive) central M&A teams within the various UK consolidators, who now find themselves with less to do in a crowded market where buyers outnumber sellers. There is a serious point to this. It has been observable over recent years that many of the larger consolidators have been increasingly willing to ‘reach down’ and do much smaller deals than they might have considered four or five years ago. This principally reflects the paucity of mid-sized targets that have been available, but is also a result of those buyers having the teams in place and capacity standing ready to do those deals. They are employing the staff, so they might as well use them to maintain momentum in their M&A strategy by working on smaller transactions, at least until some bigger ones turn up.

Specialty business remains in high demand

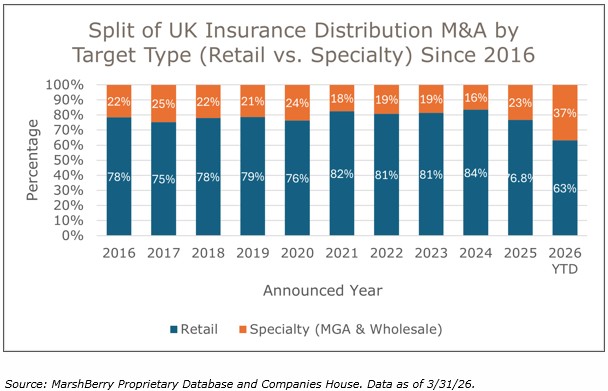

Although the volume of deals in 2026 so far is not significant enough to draw too many conclusions, the early signs are that M&A involving specialty targets (Managing General Agent (MGA) and wholesale business, including Lloyd’s brokers) will remain an important part of the story in 2026, just as they were in 2025. Year-to-date (YTD) there have seven deals (37% of all deals) involving a specialty business. There were 23 specialty deals in 2025, representing 23% of all deal volume, the highest proportion since 2020, and it remains a highly active and increasingly relevant segment of the market from an M&A perspective, with good quality targets in high demand from a wide range of range of domestic and international buyers.

The PE-backed consolidators have yet to make their mark on 2026 M&A

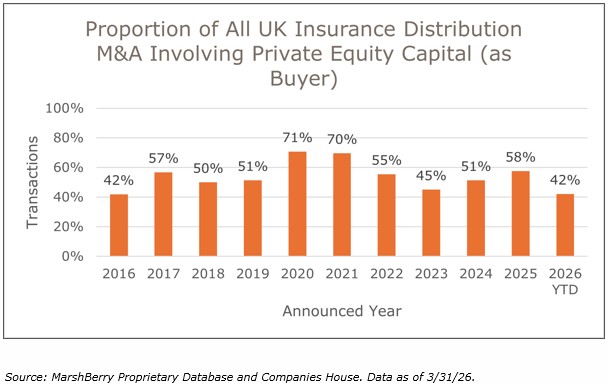

On a YTD basis only 42% of sector deals have involved a private equity (PE) or private equity-backed buyer, well below the 58% across 2025 and the longer-term average. This figure is likely to creep up over the course of the year and there remains a surfeit of PE capital in the sector that is waiting to be deployed, including from a number of sponsors who have newly entered the sector over the past twelve months, backing experienced buyers including Jensten, JMG Group and Seventeen. The YTD figure reflects the fact that several of the most active buyers in recent years have yet to announce new UK deals in 2025, but given their business models and sponsor investments, at least in commercial lines, are focused on continued inorganic growth through M&A, this will likely change. They have a continuing appetite for deals, and their well-heeled M&A teams are keeping themselves gainfully employed, across a number of large and small transactions that are expected to be announced over the coming months.

Notable transactions (March 2026):

- ANV Group Holdings, the MGA platform recently spun off from AmTrust and which already owns several UK businesses including Arc Legal, announced a deal for IRIS Insurance Brokers, the Lloyd’s broker that is best known to many commercial brokers as the owner of Blink Intermediary Solutions.

- In a deal that further consolidates the already narrow UK motorcycle segment, Principal Insurance announced a deal for Europa Group, which includes the MotorCycle Direct and Ridersure (for wholesale) brands, creating a broking group with more than £60m of GWP.

- Recently formed wholesale and MGA platform Sodalis Capital announced that it has acquired Amiga Specialty, a B.P. Marsh stablemate (and continuing investor) in a deal that reunites Colin Thompson and Adam Kembrooke, who were former colleagues at Nexus.

Other transactions (March 2026):

- Seventeen Group announced that it has acquired Smith English Insurance Brokers, a commercial broker and WTW Network member based in Cheshire.

- Bartlett James Risk Solutions acquired IPC Insurance Brokers, a fellow Momentum AR.

- PE-backed MGA consolidator Optio Group continued its recent run of deals with the acquisition of Gardian Marine, an MGA focused on marine builders risks.