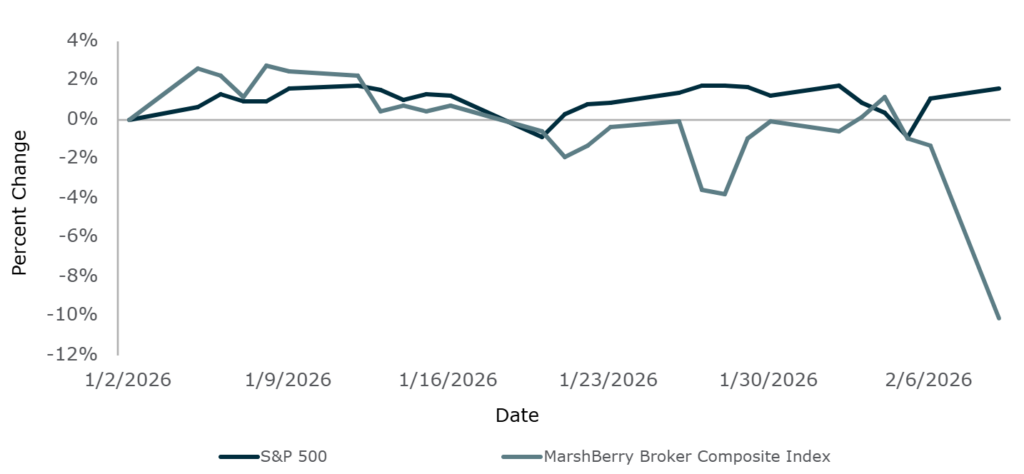

On 9 February 2026, listed insurance broking firms experienced a sharp valuation correction. In the U.S., shares of the largest broking firms saw decline – with WTW down 12%, Aon down 9.9% and Arthur J. Gallagher down 9.3% on the day. Collectively, the U.S. public brokers, as measured by the MarshBerry Broker Composite Index was down 8.9%.

Insurance Broker Stocks Fall on AI Disruption Concerns

The following day, the move rippled into European insurance stocks, with European insurance carriers such as Hiscox, MAPFRE and Admiral all losing ground on the day. The primary driver was linked to investor concerns on AI-driven insurance distribution models and their impact on traditional insurance intermediaries.

This was not a typical macro-driven swing. The catalyst was AI and, more specifically, the market’s growing belief that conversational AI is moving closer to the point of sale in insurance distribution.

This is not a moment when insurance broking becomes obsolete. It is a moment when investors reassess where value sits, how defensible customer access really is, and which firms can turn AI from a headline topic into a practical advantage.

The catalyst: AI enters the buying journey

There were two recent developments to point at as the catalyst for the market’s reaction. They both illustrated a broader shift in AI from systems that primarily write and answer questions – to AI agents that can manage a substantial part of the buying journey.

The first was a report from multiple news outlets that OpenAI approved the first insurer-built AI insurance app on ChatGPT, developed by Spanish digital insurer Tuio and powered by WaniWani’s distribution infrastructure. The app can deliver personalized home insurance quotes, directly inside ChatGPT, without the need to interact with a broker. Soon to follow will be purchasing capabilities – meaning users will be able to complete the full insurance buyer process without leaving ChatGPT.

At the same time, Insurify, a U.S.-based online insurance comparison platform, announced what it described as the industry’s first ChatGPT insurance comparison app for motor insurance. The tool enables users to compare personalised price estimates and review insurers side by side within ChatGPT, drawing on Insurify’s data and customer review base, before continuing with Insurify to complete the journey.

What sets these two developments apart from other “AI in insurance” headlines is the distribution mechanics. Through OpenAI’s App Directory, effectively an app store inside ChatGPT, third parties can embed real products and workflows directly into the conversation.

Taken together, these are clear signals that conversational AI is shifting from an information layer to an action layer. That matters because distribution economics are often shaped by whoever controls the customer’s starting point. If the first interaction happens inside an AI interface, traditional pathways built around websites, forms and separate comparison journeys become less central, and value begins to migrate towards the firms that control, integrate with, or are discoverable within that new front door.

Why markets reached for the “SaaSpocalypse” parallel

The comparison to SaaSpocalypse or SaaS-mageddon (playful uses of “apocalypse” and “armageddon”) is shorthand for a valuation dynamic seen in software markets. In the past, investors have repriced software companies as AI started to sit on top of traditional applications, weakening control of the user interface, lowering switching costs and creating pressure on seat-based subscription economics. Reuters reported a related theme in recent sell offs across software and data services, driven by fears of AI disruption and value shifting within the technology stack.

While insurance distribution is not software, the rhyme is clear. If customers increasingly begin in a conversational interface, receive guidance, compare options and move towards a quote without visiting a firm’s website or engaging a person, then the economics of attention shift. That does not automatically remove the role of intermediaries, but it does increase perceived margin pressure in segments where the value proposition is mainly access and transaction processing.

A balanced view of where AI disrupts and where it strengthens

It is important not to overgeneralise. AI’s impact will not be uniform, so it helps to separate where the buying journey is most compressible from where expertise remains central. In the near term, the clearest pressure point is in standardised, price-led journeys, particularly in personal lines, where comparison is already a familiar behaviour and where speed and convenience can outweigh relationships. In those segments, conversational AI can reduce friction, make switching easier and shift more of the early-stage customer journey into a single interface.

That dynamic looks very different in commercial and specialty lines. Much of the profit pool for large, listed intermediaries is generated in areas where risk is nuanced, coverage is bespoke and the value is created through structuring, market access, negotiation and claims support. AI can enhance these activities by improving data capture, sharpening submissions and supporting faster, better-informed decisions, but it is far less likely to turn them into a simple side-by-side comparison.

The more immediate, and arguably more consequential, shift is inside firms. As AI evolves from copilots to agentic workflows, it can take on multi-step administrative and servicing tasks across tools, escalating to people only when judgement is needed. That is not just incremental efficiency. It is capacity creation: shorter turnaround times, improved placement quality and more adviser time available for complex client work. In a market where growth is harder to generate from external tailwinds and clients are increasingly cost conscious, that operating leverage becomes a differentiator, protecting margins while enabling continued investment in expertise and client experience.

Implications for broking valuations and M&A activity

From an M&A adviser’s perspective, the recent market repricing is best read as a signal about where buyers think the value pool is heading, not a verdict on near-term trading. When investors react this sharply to distribution mechanics, it tends to foreshadow how acquirers will adjust risk assumptions, frame diligence and differentiate multiples in private markets. Three shifts are likely to become more visible in deal processes:

- Distribution resilience will be tested more explicitly. Buyers will want to understand how exposed the revenue base is to segments where AI can compress the front end of the journey, and how dependent the firm is on being the customer’s “first click”. That pushes more focus onto client stickiness, advisory intensity, and the extent to which trusted relationships are embedded beyond the transactional moment.

- Operating model capability will move up the value agenda. As conversational AI accelerates expectations on speed and transparency, investors will look harder at cost-to-serve, data quality and workflow design. Firms that can evidence AI-enabled automation in servicing, renewals and placement preparation will be viewed as better positioned to protect margins and scale. Where processes remain heavily manual, buyers are more likely to price in additional investment, execution risk and a longer path to efficiency.

- Valuation dispersion is likely to widen. Strong platforms with clear specialism, consistent organic growth and credible technology execution may continue to attract premium demand, particularly where AI is being used to release capacity and deepen client service. By contrast, firms with commoditised mixes or operational fragility may see more cautious pricing, tighter structures and greater emphasis on earn-out mechanics linked to retention and margin delivery.

The net effect is that AI becomes less a generic “tech theme” and more a concrete driver of deal outcomes. It will not replace the fundamentals that buyers have always valued, such as leadership, culture, client relationships and earnings quality. But it will increasingly influence how durable those fundamentals are perceived to be, and therefore how confidently buyers are willing to pay for growth.