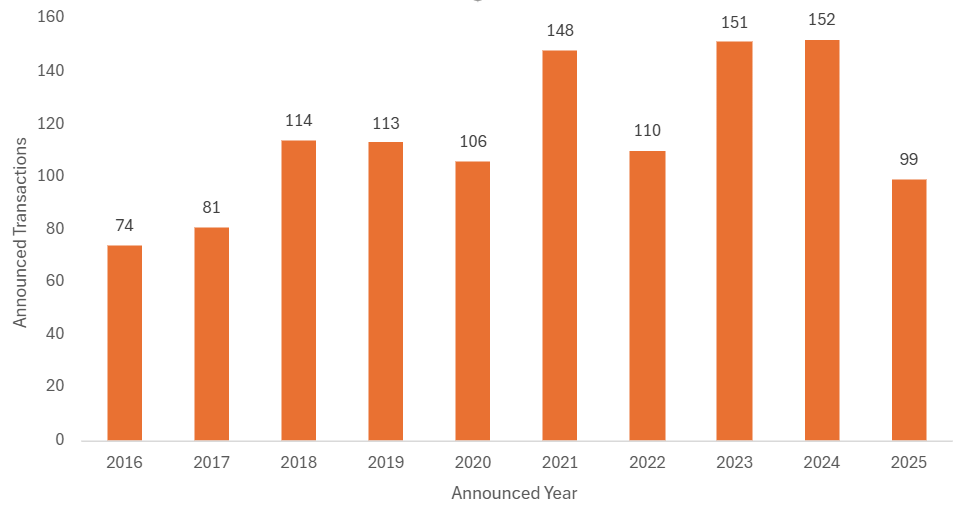

December is a ‘short’ month in terms of business days, and in the UK, there is no tax-driven motivation to close deals by year end. Historically, December has been no less active than any other month for insurance distribution mergers and acquisitions (M&A), with an average of more than eight deals a month over the past decade. However, December 2025 saw only four new deals, making it (jointly) the quietest month of 2025 for M&A, and the quietest December since 2016. It means the UK ended the year with 99 deals announced, just shy of the 100 figure that the month-on-month deal count has been broadly tracking towards throughout 2025. It also marked the first time since 2017 that the total number of sector deals in a year has not exceeded 100.

M&A Market Update

The small number of new deals announced in December left the total for the year just shy of 100, rounding out a slow year for sector M&A. MarshBerry will be publishing its annual review of sector M&A in the spring. This review will detail who sold and why, as well as looking at the overall value of M&A, including using headcount analysis to consider the changing pace of overall sector consolidation. (Spoiler Alert: both have fallen substantially.) This month’s M&A update is just a short summary of how the year ended, with a few suggestions as to why 2025 has seen such a precipitous decrease in the number of UK deals.

Total Volume of Announced UK Insurance Distribution M&A, Annual

A quiet Q4 for sector M&A

With only 22 announced deals in Q4, the last quarter of 2025 has been the quietest Q4 for sector M&A since 2016. This is in spite of a number of JMG Group’s 2025 deals falling into the quarter, as well continued activity from consistently active buyers including Partners&, The Broker Investment Group and Jensten Group. But as MarshBerry has remarked before, the story of 2025 has been of a year in which many of the most active buyers of the past 5-10 years have done significantly less M&A – Ardonagh, Brown & Brown, PIB Group, Clear, Gallagher and Seventeen Group have all been noticeably quieter over the past 12 months, at least in the UK.

But why has sector M&A fallen so rapidly? And why have the deal sizes declined? Of the 99 deals in 2025, more than half have involved a target employing fewer than 10 staff, and there were only five deals with a value of more than £100 million, the lowest since 2019. Some of this relates to supply: the fact is that there are significantly fewer mid-sized targets for consolidators to go after, but there are also demand-side explanations.

The softening rate environment has removed a multi-year tailwind from the sector, impacting organic growth. As a result, some of the larger private equity (PE)-owned businesses are having difficulties securing high-multiple exits. While valuations of publicly-traded brokers have declined over the past three quarters, with a trickle down impact on the valuations further down the food chain. Creating lasting value has become more difficult, which has introduced increased caution around acquisitions and renewed scepticism of the “pile ‘em high” M&A strategies that have characterised the recent record-breaking years of deal activity.

What will sector M&A activity in 2026 look like?

There are arguably no immediate catalysts that will likely push deal activity up to 2023/24 levels for the foreseeable future. Softening rates, debt costs that are still historically high and general macroeconomic nervousness are unlikely to fade away quickly. On the supply side, new broker and MGA (Managing General Agent) formations coming to market in 2026 won’t even scratch the surface in terms of filling demand. But on the plus side, the sector still has plenty of capital waiting to be deployed in M&A. Three UK commercial broking consolidators took on new PE capital in 2025. Overseas interest in UK insurance distribution remains buoyant (there were 15 unique overseas buyers of businesses in 2025, of which four were acquiring in the UK for the first time) and is not limited to North America. And the factors that make insurance distribution such an attractive, resilient and enduring sector – as well as the demonstrable value that a well-executed acquisitive growth strategy can deliver – are not going away.

Notable transactions (December 2025):

- In another example of a carrier divesting a distribution business, Canopius announced that its tech-led MGA Vave has been acquired by Acrisure, where it will become part of Acrisure Underwriting. Vave is a UK-headquartered MGA that uses APIs to write mainly cat-exposed business in the U.S.

- Clear Group announced that it had continued to extend its geographical reach with its first acquisition in Scotland, where it has added Cairn Corporate, a commercial broker based in Fife.

- Peter Cullum’s The Broker Investment Group (TBIG), via The Needham Group, acquired 100% of Black Lion Broking Services, a commercial broker in Surrey. TBIG has been among the most active UK buyers during the year, with only JMG Group having announced more broking deals in 2025.

Other transactions (December 2025):

- In the second deal of the month involving a Scottish target, Bain-backed Jensten Group acquired Broker One, a commercial broker in Glasgow.

* Note that the full year 2025 figure of 99 includes a small number of formally unannounced deals identified via Companies House PSC notifications and so in the public domain. We will be publishing a listing of all deals in the year involving a target reporting 10 or more staff in our annual review, available in early Spring.