After the multi-year low for insurance distribution sector mergers and acquisitions (M&A) in 2025, as measured by both deal volume and value, there were tentative signs of a pickup in activity in January, as several notable new transactions were announced. Although eight new deals in a month is still below the long-term monthly average (9.6), in January 2025 there were only four deals. More significant was the nature and size of new deals during the month, which included new direct private equity (PE) investment into a commercial broking consolidation vehicle, a network deal, and a major transaction involving an overseas acquirer. While one month is not enough to start making predictions for the year ahead, it is a positive start to the year.

M&A Market Update

There were eight new deals in January, which was twice as many as in January 2025. It is far too early in the year to divine any trends from this. Because the deal numbers are so small this early in the year, the deal numbers should be more statistically significant by the Spring and the charts at that time will show the percentage splits around retail vs. specialty and PE-backed capital vs. private capital, percentage of overseas buyers etc. The charts below look back at the overall value of sector M&A in 2025, which MarshBerry has not previously published. Our next annual M&A and market structure review, which will be available in early March, will include this data, as well as a more detailed analysis and commentary on the 2025 numbers than we have space for here.

Number of Announced UK Insurance Distribution M&A Transactions, since 2016

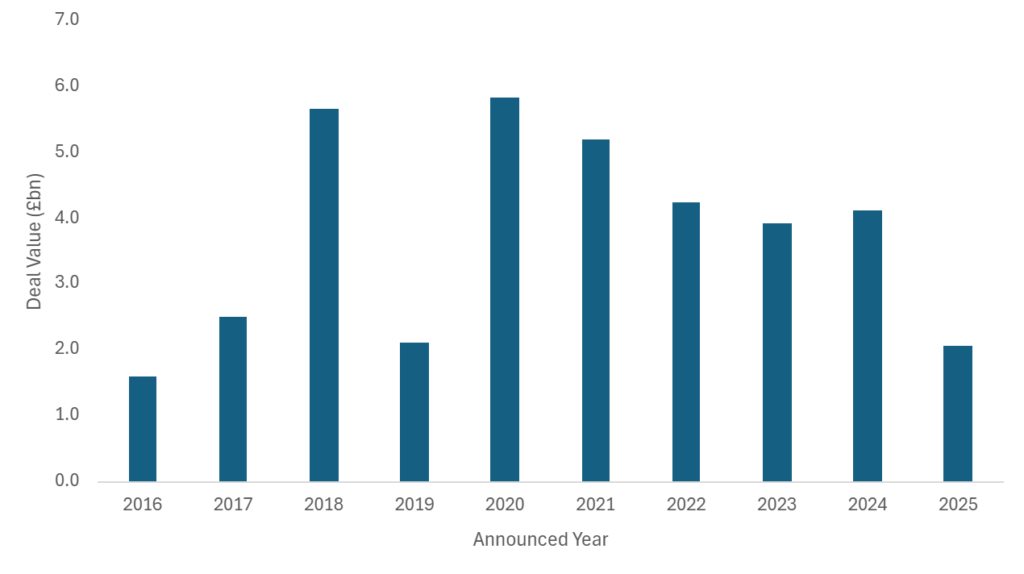

The value of sector M&A decreased in 2025

Not only were there fewer deals in 2025, but the average deal size also reduced, as it has for a number of years. Although there were a handful of large transactions in the year, mainly involving PE investment in both primary and secondary buyout deals (Seventeen Group, BPL, Jensten Group, JMG Group), there were also none of the ‘mega’ deals (>£1bn) that can really move the numbers in a given year. The result was that aggregate deal value across the 99 deals announced in 2025 was just over £2 billion, the lowest total since 2016 and around half the average deal value that sector M&A has delivered over the past three years. Of course, one or two large deals could have substantially changed this – think PIB Group’s aborted deal with Gallagher at a rumoured valuation of more than £3 billion – and so it is a poor barometer of the level of underlying sector M&A activity, but it does reinforce the fact that 2025 saw a marked pullback in deal activity. In January 2026 there has already been one deal valued at above £100m (AUB Group’s £219m deal for Prestige) and as sector consolidation results in bigger and bigger groups that are typically backed by PE investors who are by their very nature only temporary owners, the overall value of sector M&A will remain concentrated across a small number of very large deals.

Deal Value of announced UK Insurance Distribution M&A (all deals) 2016-2025 – in £bn

Will January set the tone for the rest of 2026?

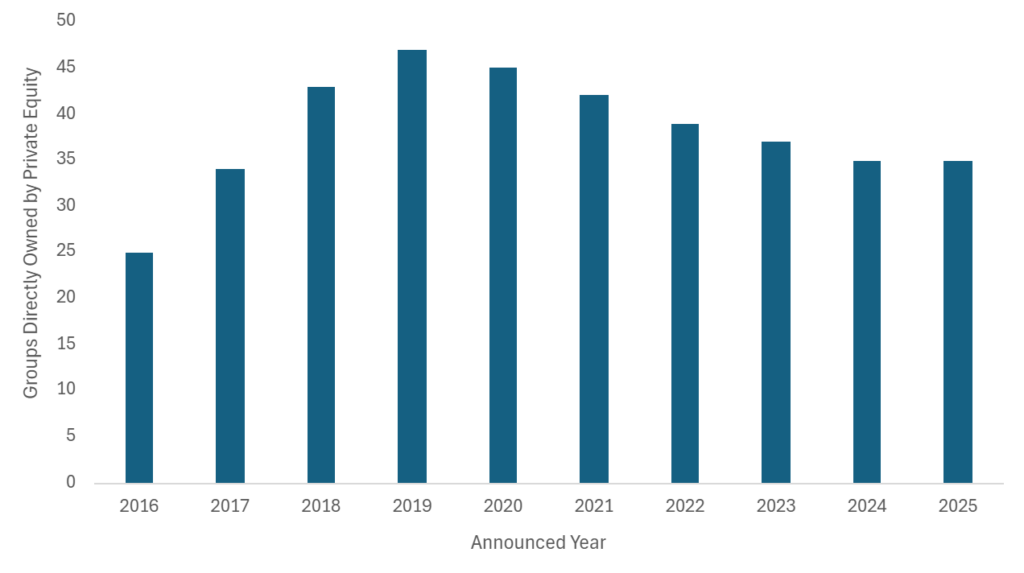

January’s deals highlight two themes that were in evidence throughout 2025 and are set to continue in 2026. Inflexion’s investment in Ascend brings further fresh capital to the sector to support domestic consolidation in commercial broking, and will further increase competition amongst a buyer universe chasing a decreasing number of privately-held commercial broking targets of scale. Capital Z’s exit of Prestige to a trade buyer, AUB Group, sees PE capital coming out of the sector, but again highlights the attractiveness of the UK market to larger overseas groups with an international growth strategy. There were 35 insurance distribution groups directly held by PE investors at the end of 2025, the same number as at the beginning of the year (following five new investments and five divestments during 2025). Several of these will be put up for sale in 2026, with buyer interest expected to come from PE (i.e., secondary deals), other domestic consolidators, and overseas trade/strategic. Watch this space.

No. of UK insurance distribution groups directly owned by Private Equity

What to expect in 2026

MarshBerry has previously noted that several of the factors that suppressed deal volumes in 2025 – a lack of supply of mid-sized targets, softening rates removing an industry tailwind (and in turn dampening valuations of the publicly listed broking groups in the U.S.), and macroeconomic uncertainties – will not reverse overnight, and as such there are few immediate catalysts for an immediate uptick in M&A volumes. It is not all doom and gloom however. Capital to support industry consolidation remains plentiful, with recent new PE investment-backed buyers focused on domestic M&A. The UK remains an attractive market on the radar of many overseas groups. Industry fragmentation, at least at the smaller end, remains high, with ageing owners that will need to sell. And new businesses continue to be formed – particularly in the specialty segment, where the rise and rise of MGAs (Managing General Agents) shows few signs of slowing. Deal activity is unlikely to bounce back to 2023/24 levels in 2026, but sector M&A isn’t going away.

The increased caution that characterised 2025 is likely to persist in 2026, with PE investors that have bought in at high multiples remaining nervous about their ability to generate hoped-for returns in the current environment. Public market valuations will trickle down to impact deal pricing for brokers further down the chain. Reduced valuations will impact staff equity owners, which risks weakening the ‘glue’ that can hold some groups together. The recent failure of some larger groups that had not fully integrated acquisitions to attain premium valuations on their sales will continue to push owners and management teams to focus more on integration, and in turn may encourage a more selective approach to M&A.

MarshBerry will continue to monitor and report on these trends, both in the UK and across our markets. If you would like to discuss the changing M&A environment or speak to an expert about your own business, we would love to hear from you.

Notable transactions (January 2026):

- Mid-market PE firm Inflexion, which has previously backed both Bollington Wilson and DR&P, announced it would be again investing in the UK commercial broking segment with ambitious plans to build out a new broker platform, using Ascend Broking Group as an anchor investment.

- Clear Group announced two new deals in the month, adding veterinary sector specialist Shire Insurance Services which will become part of its retail division, and Gauntlet, comprising Gauntlet Retail Brokers and The Gauntlet AR Network, a principal for Appointed Rep insurance brokers that it is envisaged will help develop Clear-owned network Brokerbility.

- Australian-listed AUB Group, which already owns Tysers and Movo in the UK, announced the acquisition of PIHL Holdings, the parent company of Prestige Insurance, in a deal valued at £219 million. Prestige operates across broking, MGA business and technology, across several brands and multiple locations. It will serve as AUB’s principal UK retail broking platform. The business has been backed by specialist PE investor Capital Z Partners since 2018.

Other transactions (January 2026):

- Nexus Underwriting, part of Brown & Brown (Europe) announced the acquisition of Sure Insurance Services, a specialist in cover for medical tourism.

- Partners&, one of the Top 10 most active buyers in 2025, continued its recent run of deals with the acquisition of STP Risk Solutions, a commercial broker in Hull.

- Specialist Risk Group announced the acquisition of commercial broker Kennett Insurance & Risk Management, also in Hull. SRG acquired the business from WF Risk Group, from whom they previously acquired Generation Underwriting in a deal announced in 2025.

- It was reported (by Matt McColl) that Matt McColl, the founder and CEO of recycling and waste specialist Raw Material Cover had reached an agreement to acquire Lothbury UK, the Lloyd’s broker.