In what seems to be an ever-present challenge within the insurance retail industry, many firms today continue to wrestle with a familiar problem: producers who carry the title without generating the production. Whether they’re legacy performers who have slowed down or newer hires who never fully validated, these non-producing producers represent more than an isolated issue. Obviously, they can hinder overall organic growth, but they can also weaken a firm’s performance standards and even dilute culture.

The solution for addressing the “non-producing producer” is not simply to push harder or place them on a performance improvement plan (PIP), but to build a system where expectations are understood, measured, and enforced, and where support, consequences, and opportunity all work together to drive results.

What does success look like?

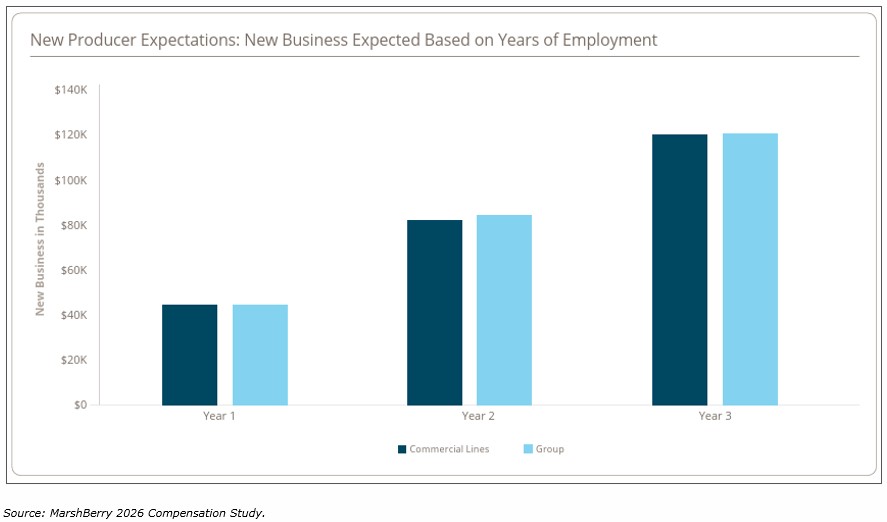

MarshBerry’s 2026 Insurance Agency & Brokerage Compensation Report reveals what top-performing firms are doing to remain competitive. High-performing firms don’t leave productivity open to interpretation. They clearly define expectations up front. At its core, the role of a producer is to generate new business opportunities that otherwise would not exist for the firm. That expectation must be translated into tangible, measurable goals at the individual level. As this chart reflects, Compensation Survey participants revealed that by the third year, new producers are expected to deliver approximately $125K in new business (for both commercial lines and group benefits).

Effective producer goal frameworks typically include:

- Minimum goals – the baseline requirement to maintain producer status.

- Individual goals – realistic targets based on experience and market opportunity.

- Stretch goals – aspirational outcomes that reward top performers.

When these goals are paired with regular performance reviews and consistent communication, they become operational expectations. The data is clear: Firms that define goals, monitor performance, and take timely action consistently outperform those that do not.

Accountability: the missing link in many organizations

Even when goals are established, they’re not always enforced, and expectations without accountability can become optional. According to MarshBerry data, accountability mechanisms vary widely – from PIPs to compensation adjustments to role changes – but for a meaningful percentage of firms there are no consequences for underproducing.

This lack of follow-through creates a dangerous precedent: expectations become optional. To truly drive productivity, accountability must be structured and predictable. That includes:

- Minimum annual new business thresholds.

- Minimum account thresholds.

- Regular performance tracking (quarterly at minimum).

- Defined consequences for underperformance.

- Timely intervention – not reaction well after the fact.

Most importantly, accountability must be tied directly to the outcomes that matter most: new business generation and profitable growth.

Aligning compensation with the right behaviors

Compensation remains one of the most powerful levers to positively influence producer behavior. To make maximum impact on the business, however, compensation must be aligned with the firm’s growth strategy.

Here are the two fundamental principles: Compensation should reward new business generation, and compensation should not over-reward servicing existing accounts. MarshBerry’s research reinforces this distinction with data suggesting a 15-20 percentage point difference between new and renewal commission rates to encourage producers to prioritize growth. Firms that fail to create this differentiation often see producers gravitate toward maintaining existing business rather than generating new revenue. To help producers maintain that new-business focus, firms must reinvest dollars into the service and support structure to serve as the primary point of contact for the insured. This creates capacity for producers to focus on generating new business, and it also serves to institutionalize the account.

Making the tough call: role realignment

Even with clear expectations, mechanisms for accountability in place, and compensation aligned with the firm’s goals, not every producer will succeed. The highest-performing firms recognize this and act accordingly. For individuals who consistently fail to meet production expectations, one of the most effective strategies is role realignment. Moving a non-producing producer into an account executive or service role can often:

- Preserve valuable client relationships.

- Improve operational efficiency.

- Allow individuals to contribute in a more suitable capacity.

- Protect the integrity of the sales culture.

Service roles, particularly account executives, are critical to the success of any brokerage as they handle complex accounts and help ensure retention. By placing the right people in the right roles, firms can improve both productivity and morale.

Building a culture that produces

Ultimately, improving producer productivity is not about a single tactic. It’s about building a system in which expectations are clearly defined, goals are measurable and visible, compensation reinforces the best behaviors, accountability is consistent, and both opportunities – and consequences – are real. Firms that embrace this structure reduce the presence of non-producing producers, but they also create a culture in which production is contagious. And in a competitive environment where growth is increasingly hard-won, that culture may be the most valuable asset of all.

The value of a compensation study

MarshBerry’s comprehensive, one-of-a-kind industry report evaluates compensation trends across multiple roles in insurance brokerage. It provides over 100 charts illustrating respondent data and detailed insights into the results. The report allows insurance brokerages to benchmark where their firm sits in the range of industry peers on compensation approaches. It can reinforce their current approach or reveal areas for change.

As insurance brokerages continue to look for ways to grow their business, whether through their product offerings, service capabilities, or technology upgrades, people will always be at the root of everything they do. Having a top-performing organization with top-performing personnel starts with a top-performing compensation strategy.

Learn more about MarshBerry’s 2026 Insurance Agency & Brokerage Compensation Study.