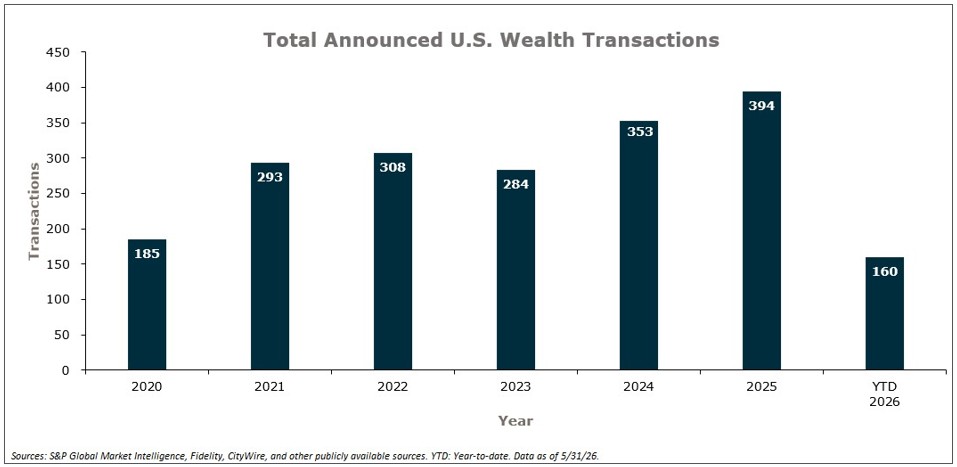

Wealth management merger and acquisition (M&A) activity continued to build momentum through May, with 40 announced transactions added during the month – bringing the year-to-date total to 160 transactions. This represents an 11.1% increase over May 2025 year-to-date activity, which totaled 144 announced deals, underscoring the continued strength and resiliency of the market. Despite periods of broader economic uncertainty and market volatility, buyer appetite remains robust as both strategic and financial acquirers pursue opportunities to expand scale, enhance capabilities, and deepen their presence in attractive markets. Sellers, meanwhile, continue to evaluate partnerships that can support succession planning, strengthen infrastructure, and position their firms for long-term growth. The strong pace of activity through May reinforces the durability of the wealth management consolidation trend and the continued confidence buyers have in the sector’s long-term fundamentals.

M&A market update

Private capital-backed buyers accounted for 110 of the 160 transactions (68.8%) through May, down from the 2025 year-end figure of 74.0%. Independent firms accounted for 41 deals and 25.6% of the market, which is an increase from 2025’s final percentage of 20.0% (on 86 total independent deals). Insurance brokerages acquired six wealth management and retirement firms in 2026.

The top 10 buyers represented 34.4% of total transactions, and the top three acquirers (Hightower, Carson, and Savant) accounted for 13.8% of all announced deals. At the same time, geographic dispersion reinforces the breadth of the current market environment. A total of 39 states recorded wealth management M&A activity through May, with California leading the country at 15 transactions, underscoring both the depth and national reach of ongoing consolidation.

Notable transactions:

May 5: Wealthspire agreed to acquire Fi3 Advisors, an Indianapolis-based boutique wealth management firm overseeing approximately $1.2 billion in assets under management, further expanding its presence in the high-net-worth and ultra-high-net-worth market. The transaction builds on a longstanding relationship between Fi3 and Fiducient Advisors and enhances Wealthspire’s ability to deliver family office services, including advanced tax and estate planning, trust services, and family office administration. Founded on a family office-style advisory model, Fi3 has established a reputation for highly personalized client service and will continue to operate under its existing leadership team following the transaction. Combined with Wealthspire’s recent acquisition of Axia Advisory, the deal significantly expands the firm’s scale in the Indianapolis market and supports its broader strategy of serving increasingly complex client needs through an integrated wealth management platform.

May 20: Bluespring Wealth acquired Synthesis Wealth Planning, a New Jersey-based wealth management firm overseeing approximately $1.1 billion in assets following its combination with fellow Kestra-affiliated firm IFG Wealth Strategies. Founded in 2018, Synthesis has grown from roughly $200 million in assets through a combination of organic growth, advisor recruitment, and strategic acquisitions, while maintaining a planning-led approach centered on financial planning, portfolio management, and insurance solutions. The transaction expands Bluespring’s presence in the Northeast and Florida, adding offices across New Jersey and Florida, and provides Synthesis with access to additional operational resources, infrastructure, and growth support. The acquisition continues Bluespring’s strategy of partnering with entrepreneurial wealth management firms that have demonstrated strong organic growth and scalable client service models. MarshBerry served as advisor to Synthesis Wealth Planning in this transaction.

Looking forward

Looking ahead, wealth management M&A activity appears well positioned to maintain its positive momentum. Through the first several months of the year, deal volume has continued to outpace the prior-year period, highlighting the ongoing strength of consolidation across the sector. Much of the activity taking place today is the result of thoughtful strategic planning that began well before transactions were announced, as firms assessed the resources, scale, and infrastructure needed to meet shifting client demands and operate more efficiently in an increasingly complex environment. As 2026 continues, the market remains underpinned by substantial capital availability, a deep pool of active acquirers, and a growing understanding that the right partnership can help accelerate growth, enhance competitiveness, and preserve long-term enterprise value.