Everybody uses technology. Yet even though tech integration is universal across the insurance distribution industry, its impact is frequently constrained by a tendency to prioritize operational efficiency enhancements over solutions that can increase revenue.

A perplexing discovery

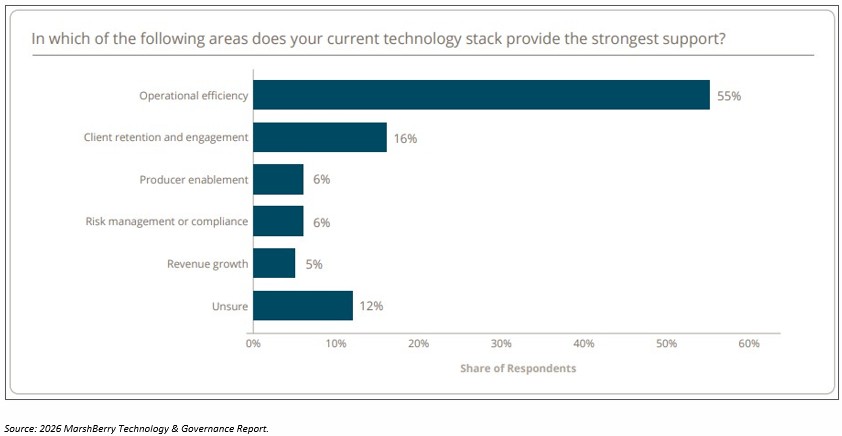

MarshBerry’s 2026 Technology & Governance Report reveals that a majority of firms (55%) feel their current tech stack makes its greatest contribution to operational efficiency – while a shockingly low 5% of respondents state that their technology makes its strongest contribution relative to revenue growth.

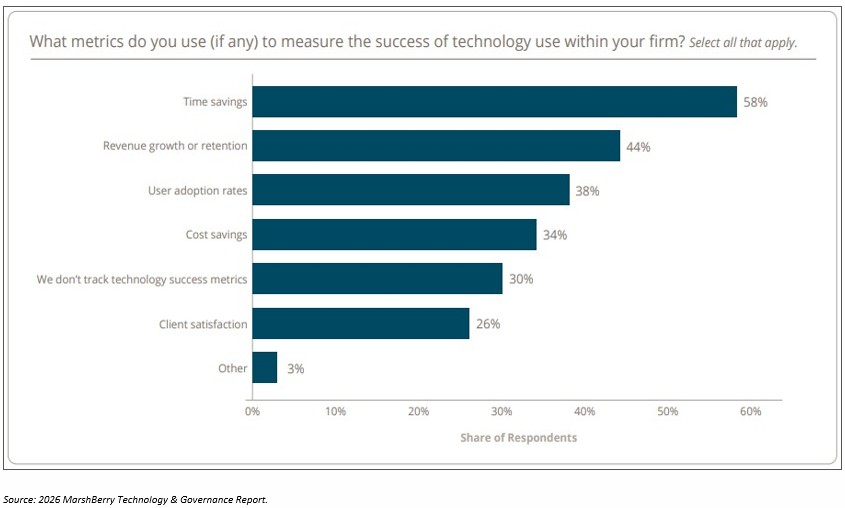

To add even more paradoxical perplexity to these already interesting results, when asked how they measure the success of their technology implementation, operational efficiency (aka “time savings”) still came in first – but 44% of respondents reported that revenue growth was the second most important metric! How can 44% of firms believe that revenue enhancement is such an important metric while only 5% believe that their technology is making its greatest contribution in that area?

In other words, the second most important measurement of success (revenue growth) is not actually contributing to that goal.

A structural problem

The explanation for these surprising statistics is not a lack of tools or even a lack of awareness. Instead, the challenge lies in how firms apply technology. Many organizations continue to operate with fragmented systems, inconsistent data, and loosely integrated workflows. As a result, technology investments tend to produce incremental improvements rather than meaningful, enterprise-wide impact. In short, firms are structured in such a way that they search for efficiency within silos, rather than rethink how technology can transform the way their entire business grows.

Firms consistently define the success of technology in terms of internal efficiency – how much faster work gets done, how much manual effort is eliminated, and how smoothly operations run. These are all worthwhile outcomes, but they are inherently back-office measures and not necessarily contributing meaningfully to bottom-line growth metrics.

It’s time to shift the mindset

Here’s another interesting inconsistency: While most firms are still operating with a “technology equals efficiency” mindset, they view technology’s potential quite differently. When asked where improved technology would make the biggest impact, firms point overwhelmingly to sales enablement capabilities:

- Quoting and proposal generation tools (67%)

- CRM usability and integration (56%)

- Account intelligence and segmentation tools (52%)

- Pipeline management (42%)

- Onboarding and training (25%)

- Mobile access to client and prospect data (20%)

This is perhaps the most important insight within the data. When firms step back from how they currently measure technology and instead consider where it could have the greatest impact, their focus shifts immediately from the back office to the front-line producer. This reveals a fundamental disconnect.

Firms are investing in technology to solve operational challenges – and measuring success accordingly – while simultaneously acknowledging that the greatest opportunity exists in improving producer productivity.

Taking new steps in the right direction

To close this gap between what is happening and what firms believe should be happening with technology adoption, leaders must rethink how technology is deployed and how success is defined. Here are three steps to start moving in a new – and better – direction:

1. Reframe technology as a growth engine

Efficiency gains are valuable, but they are finite. There’s only so much time to be saved or cost that can be reduced. Revenue, on the other hand, scales. Technology investments should be evaluated through a simple lens: Does this technology help producers sell more, sell faster, or sell better? In other words, does it contribute directly to revenue growth? If the answer is no, the impact – regardless of efficiency gains – will be limited.

2. Prioritize producer-facing capabilities

This is where technology can drive the most value in the sales process:

- Faster, more accurate quoting and proposal generation.

- CRM systems that are fully integrated and fully leveraged.

- Access to actionable account intelligence and segmentation.

- Clear visibility into pipeline activity and conversion.

These are not finite, incremental improvements. They are efforts that directly influence performance indicators such as new business conversion (i.e., “hit ratios”), the amount of time it takes to move from initial prospecting/quoting to closing (i.e., “cycle times”), and average account size. They are all leading indicators of revenue growth whose impact, theoretically, has no ceiling.

3. Shift from lagging to leading metrics

Directly related to the implementation of producer-facing tech, firms should incorporate leading, growth-oriented measures, such as: producer activity levels (calls, meetings, proposals); cycle times; sales velocity; revenue per producer; and hit ratios. Because firms continue to view technology as a creator of efficiency, most metrics track lagging indicators like time savings or cost reduction. The new metrics align technology performance with business outcomes, creating measurable accountability for growth.

Getting priorities aligned

The insurance distribution industry is not lacking in technology. Nor is it lacking intent. But the statistics show that there is a misalignment between implementations and aspirations when it comes to getting the most from technology. To fix this, the best-positioned firms will align technology strategy with growth strategy rather than operational efficiency. Their tech metrics will connect with business outcomes, and operational efficiency will be measured in relation to revenue generation. In the end, the best way to use technology is not simply to run the business better. It’s to grow it faster.