Insurance brokerage mergers and acquisitions (M&A) in 2026 reflects a market that remains structurally strong but more disciplined and selective than in prior years. While the market remains active, transactions activity continues to trail last year’s pace. With broader macro uncertainty in 2026 – which includes elevated borrowing costs, continued geopolitical volatility, and now energy price pressure – there is a more cautious dealmaking environment, particularly for buyers that rely heavily on leverage.

Strategically, the market continues to shift toward quality over quantity. Buyers are prioritizing niche expertise, organic growth potential, and operational fit, while also emphasizing integration and value creation post-close. At the same time, macro pressures – higher interest rates, slower organic growth, and tighter financing – are tempering large, highly leveraged deals.

High-quality firms with strong organic growth, specialty capabilities, and durable margins should continue to command strong interest and elevated valuations, while weaker or more rate-dependent firms may face a tougher valuation environment.

The concentration of deal activity among the most active buyers also suggests scale, available capital, and conviction remain major advantages in the current market.

Overall, 2026 brokerage M&A is best characterized as resilient but recalibrating: a consolidation story still in force, driven by abundant capital and strategic necessity, but increasingly defined by selectivity, discipline, and long-term value creation.

M&A Market Update

As of May 31, 2026, there were 241 announced M&A transactions in the U.S. This is down 5.1% compared to last year at this time when there were 254 transactions announced through May.

Private capital-backed buyers accounted for 170 of the 241 deals (70.5%) through May. Independent brokers were buyers in 23 deals, representing 9.5% of the market. There have been five announced transactions by bank buyers in 2026.

Deals involving specialty intermediaries as targets accounted for 46 transactions, representing 19.1% of all deals so far – a continued uptick in activity for a sector of sellers that has been in low supply for a few years.

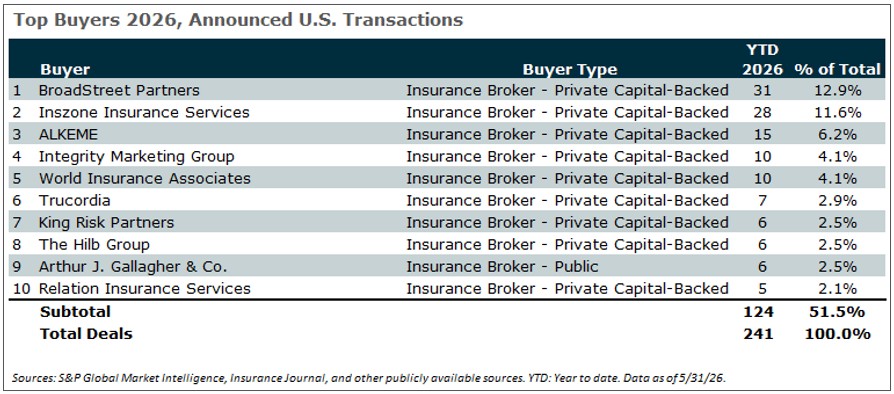

Deal activity from the top ten buyers accounted for 51.5% of all announced transactions, while the top three (BroadStreet Partners, Inszone, and ALKEME) accounted for 30.7% of the 241 total transactions.

Notable Transactions:

- May 1: BroadStreet Partners acquired Bearing Insurance Group, a Virginia-based independent insurance brokerage with roots dating back to 1999. Headquartered in Glen Allen, Virginia, Bearing provides a broad range of commercial and personal insurance solutions, including property and casualty, employee benefits, workers’ compensation, and business auto coverage. Originally established by a consortium of community banks and rebranded as Bearing Insurance Group in 2024, the firm has built a strong presence across the Mid-Atlantic through its client-focused approach and diversified service offerings. The transaction adds another established regional platform to BroadStreet’s growing network of partner agencies and further expands its footprint in the Southeast and Mid-Atlantic insurance markets.

- May 1: Hub International acquired Johannesen Farrar Insurance Agency (JFI), a Delavan, Wisconsin-based multi-line insurance agency with a long history serving clients across the state. Founded in the mid-1900s, JFI provides a range of commercial and personal insurance solutions and has built a strong presence in its local market through longstanding client relationships. The transaction gives JFI access to Hub’s broader resources, carrier relationships, and national platform, while enhancing its ability to serve commercial clients through expanded capabilities, including employee benefits offerings. The acquisition further strengthens Hub’s presence in Wisconsin and aligns with its strategy of partnering with established community-based agencies.

2026 Acquisition Detail (YTD as of May 31, 2026)

Retail vs. Specialty:

- Retail: 195

- Specialty: 46

What’s Being Bought:

- Full Service: 26

- P&C: 173

- Employee Benefits: 42

Who’s Buying

- Insurance Broker – Independent: 23

- Insurance Broker – Public: 22

- Insurance Broker – Private Capital Backed: 170

- Insurer and Other: 21

- Bank & Thrift: 5