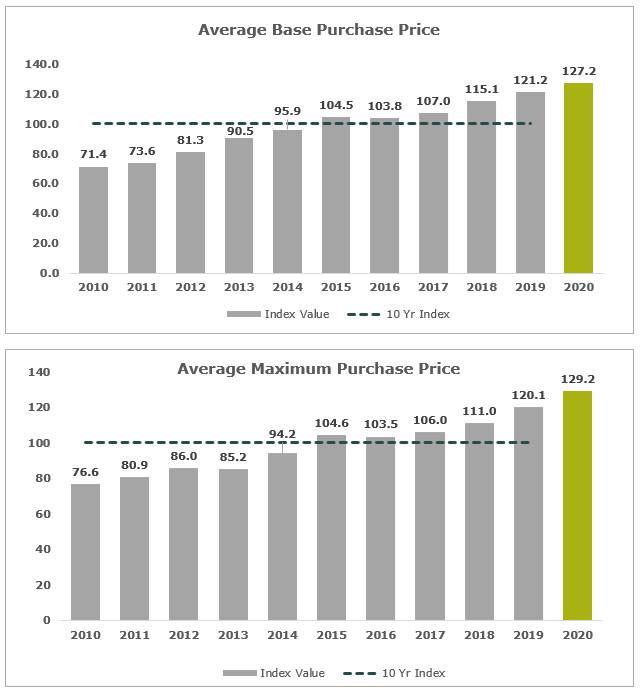

The average annual and rolling last twelve-month valuation data from MarshBerry’s proprietary database tells a consistent story.

2020 was a roller coaster in many ways with ups and downs around quarantines, office openings and closings, and a corkscrew economy. However, when it came to merger and acquisition (M&A) activity, 2020 was more like waiting for a long train at a railroad crossing vs. the twisting and turning roller coaster experienced by many other industries.

The year started at full speed in the M&A environment. When the country went into full scale lockdown deals were put on hold, valuations were uncertain, and no one was willing to predict when it would end. Buyers and sellers were in a wait and see environment.

Looking back, the average annual and rolling last twelve-month valuation data from MarshBerry’s proprietary database tells a consistent story.

Through early fall, it appeared as if multiples had leveled off at the values seen in 1Q20. However, when the data is rolled forward another three months to the end of 2020 in a 12-month view, there is a fairly significant step up in valuations, both on the “base1” (aka “upfront”) purchase price and on the maximum2 deal value including all possible earnouts. In total, maximum deal value for the average transaction is up almost 30% compared to the 10-year average, with a slight outgrowth in the maximum value as compared to the base purchase price. This indicates that more recently there has been an increased shift towards contingent consideration.

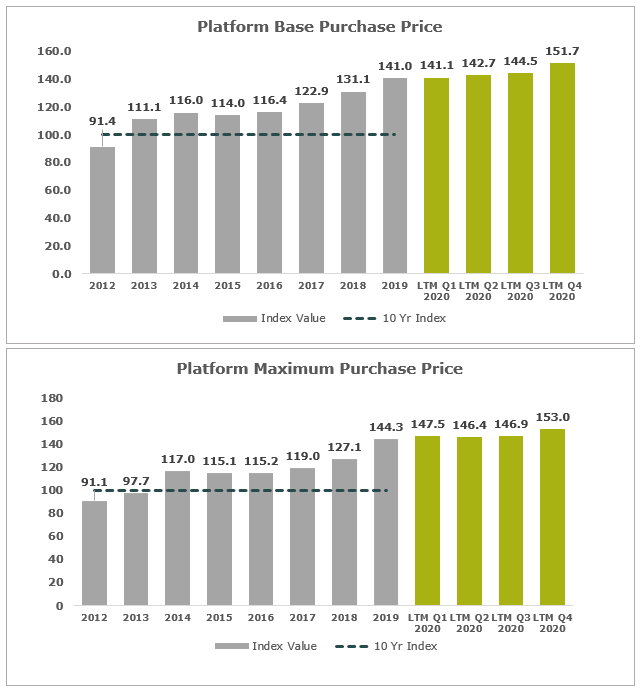

As displayed below, when it comes to “Platform3” transactions, deal values were up more than 50% throughout 2020 as compared to the 10-year average. Since 2017, Platform deal values are up almost 30% through 2020.

With 2020 in the rearview, we now see that the COVID-19 economic fallout did not materially change buyer appetite, pricing, or seller interest in external sales. There are pending events on the horizon that may impact the market (e.g. tax changes, interest rate hikes, etc.). The insurance industry fundamentals continue to be strong and the insurance distribution industry remains a highly sought after investment. Will 2021 be more like waiting on a long train at a railroad crossing, the twisting and turning of a roller coaster ride, or a bullet train of activity?

If you have questions about Today’s ViewPoint or would like to learn more about recent M&A activity, please email or call Phil Trem, President – Financial Advisory, at 440.392.6547.

Subscribe to MarshBerry’s Today’s ViewPoint blog for the latest news and updates and follow us on social media.

1The amount of proceeds paid at closing, including any escrow amounts for indemnification items, (i.e., Paid at Close) plus amounts that the buyer may initially hold back, but which are paid as long as the sellers performance does not materially decline, or which may be paid at closing but are subject to a potential adjustment (i.e., Live Out).

2The additional earn out above the realistic level, that if achieved, would generate the maximum possible earn out payment

3A Platform agency is typically a larger agency that has a well-established territory, brand recognition, seasoned professionals, and a scalable infrastructure, among other attributes. The buyer of a Platform agency is typically looking to establish a presence in a specific region or niche.

Sources: MarshBerry proprietary database. Data compiled from transactions in which we were directly involved, those from which we have detailed information, and transactions in the public record. Numbers may not add due to rounding. Past performance is not necessarily indicative of future results. Individual results may vary. LTM: Last Twelve Months; Q1: Quarter 1; Q2: Quarter 2; Q3: Quarter 3; Q4: Quarter 4; EBITDA: Earnings Before Interest, Taxes, Depreciation, and Amortization.

Investment banking services offered through MarshBerry Capital, Inc., Member FINRA Member SIPC and an affiliate of Marsh, Berry & Company, Inc. 28601 Chagrin Boulevard, Suite 400, Woodmere, Ohio 44122 (440.354.3230)