As the insurance landscape experiences ongoing inflation, climate volatility, and expanding litigation trends, traditional admitted carriers are reducing exposure to underperforming or hard-to-place risks. Consequently, the Excess & Surplus (E&S) market has become a formidable competitor in the property and casualty (P&C) landscape.

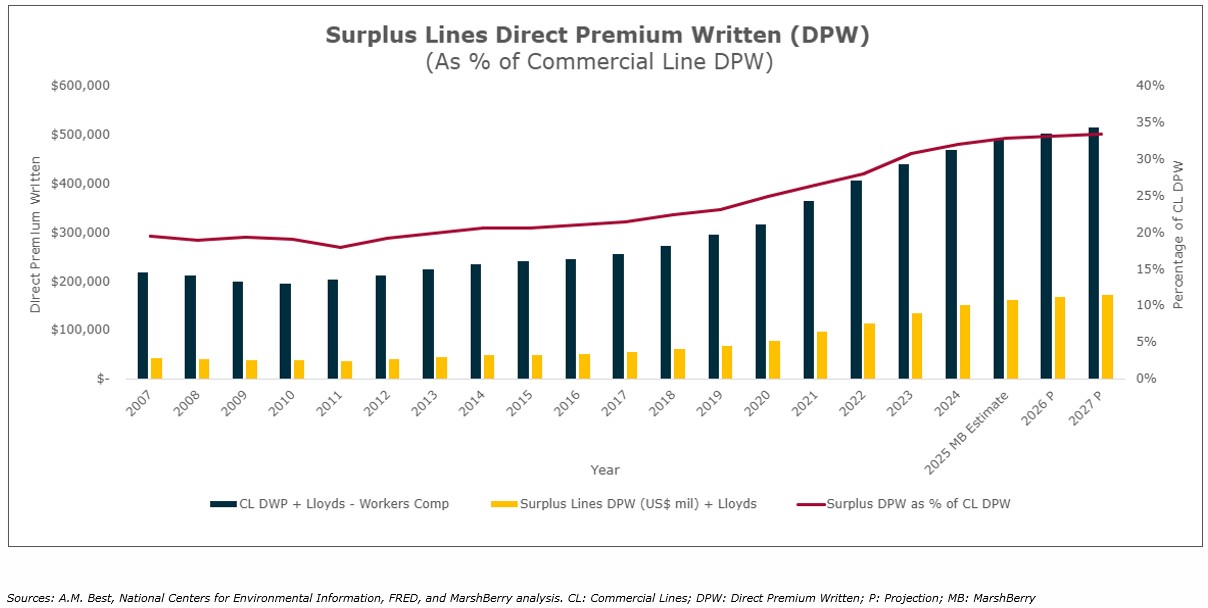

Over the past ten years, the E&S market has grown 223%, expanding from $40 billion DPW (direct premium written) in 2014 to $130 billion DPW in 2024, three times as fast as the broader P&C market’s growth of 86% over the same period. E&S premium volume is projected to reach $140-145 billion in 2025, capturing an estimated 35 cents of every premium dollar in the domestic commercial P&C market.

E&S is expected to see more measured growth in 2026

The E&S sector is expected to continue expanding in 2026 and be a viable and often preferable alternative to the admitted market for many lines of business, particularly those focused on emerging risks. The core advantages of E&S, including nuanced risk selection, pricing flexibility, and the ability to exclude underpriced or uninsurable risks are likely to help fuel its future growth.

While pricing momentum has slowed as broad-based rate increases have begun to moderate, particularly in property and select professional lines, the structural drivers of E&S growth remain, including ongoing admitted market retrenchment, nuclear verdicts related to social inflation, elevated catastrophe losses, and continued demand for flexible underwriting solutions. As a result, premium growth is resulting from exposure-driven and underwriting-driven expansion.

One of the key reasons for the E&S market’s continued growth is its underwriting strength. When E&S carriers generate lower loss ratios and stronger underwriting profits than the broader admitted market, capital tends to flow toward the segment.

From 2010-2014, E&S carriers maintained a 3.8 percentage point advantage (based on the 5-year average) in loss ratios compared to the admitted market. During this period, the admitted market’s net loss and LAE (loss adjustment expense) ratio was 72.8% (5-year average), compared to the E&S market’s 69%. By 2020-2024, that gap had widened to 8 percentage points or more than double. By 2020-2024, the admitted market had a 73.3% net loss and LAE ratio, compared to the E&S market’s 65.6%. Combined ratios consistently showed superior profitability, reinforcing the value proposition of E&S capacity, especially in an environment marked by volatility and inflationary pressure.

How Emerging risks are redefining the E&S Insurance market

In 2016, emerging risks included issues like distracted driving, aging workforce, and drones. Cyber risks were just beginning to emerge, with most of the risk being covered in the admitted market. Cyber coverage has now shifted to the surplus lines market, where 65% of such coverage is currently provided.

Today, there are very different emerging exposures that are rapidly reshaping the risk landscape and creating underwriting complexity. Here are some of those emerging risks:

- Artificial Intelligence (AI) liability, including issues around algorithmic bias, misuse of large data sets and copyright infringement.

- Driverless vehicles, whose technological problems can contribute to accidents without driver error.

- GLP-1 weight loss drugs and similar medications, which can cause potentially adverse health effects, including bone density issues and other health concerns.

- Social media/influencer liability, including instances where influencers are sued by designers and companies such as Prada after the influencers sell and promote their counterfeit luxury goods.

- Commercial drones, which are increasingly being used in agriculture, real estate, construction and logistics, have created the need for insurance to cover risks like liability and property damage.1

- The regulation of harmful or objectionable online content, including challenges around moderation standards, platform liability, and evolving legal requirements.

- Parametric insurance solutions, including products that provide rapid, transparent payouts for weather-related, seismic, and business-interruption events for which an actual loss does NOT have to be substantiated.

These risks are expected to generate strong demand for tailored E&S solutions in areas that the admitted market is unable to address.

E&S Market Opportunities for MGAs and program administrators

With its more flexible regulatory framework and increasingly data-driven underwriting models, the E&S carrier marketplace is well-positioned to support continued growth in non-standard risks, especially as market volatility, litigation trends, and capital constraints continue to challenge the admitted market. With the surplus lines market commanding a growing share of total premiums and delivering superior underwriting results, managing general agents (MGAs) and program administrators have an opportunity for greater growth and market share, driven by robust capacity from E&S carriers, and an increasing willingness from investors to back delegated authority models.

MarshBerry’s Peak Performance Summit

This article is based on a presentation given at this year’s Peak Performance Summit, an invite-only event for insurance industry leaders that provides unique networking opportunities while learning about the most significant trends and challenges impacting the specialty insurance intermediary market.