After 2025 produced the third highest M&A total on record — with 854 insurance brokerage deals announced — the natural question is whether 2026 can sustain that momentum. So far, the opening months of the year look very similar to the pattern set in early 2025: an environment defined by economic uncertainty, stubborn inflation, elevated borrowing costs, a cooling labor market, geopolitical tension, shifting trade dynamics, and an unsettled political landscape.

Layered on top of this is a major new global headwind: escalating conflict in Iran which has injected fresh volatility into global markets. This sudden geopolitical shock has been significant, triggering immediate energy market disruptions, with Brent crude (one of the world’s major benchmark prices for oil) jumping 8–13% in early March. Analysts are already warning that a prolonged conflict could add meaningful upward pressure to consumer prices and heighten recession risks.

Consequences of this turbulent economic environment include sharp swings in financial markets, a Federal Reserve that continues to hold rates steady, and M&A activity that feels increasingly cautious and deliberate.

For potential acquirers, capital remains available, but it’s still expensive — which may slow deal volume and push buyers, especially those dependent on leverage, to tighten their criteria. Still-too-high capital costs may not dramatically alter momentum or overall volume, but could redefine who participates, at what price, and under what structure. Weaker balance‑sheet buyers may be sidelined, even as valuations for high‑quality brokerages remain elevated due to limited supply and ongoing demand from private capital-backed platforms.

If 2026 ends up mirroring 2025 in both economic stability and dealmaking pace, most market participants would view that as a favorable outcome. But the balance is delicate, and even a modest shift in conditions could move the industry meaningfully in one direction or the other.

M&A market update

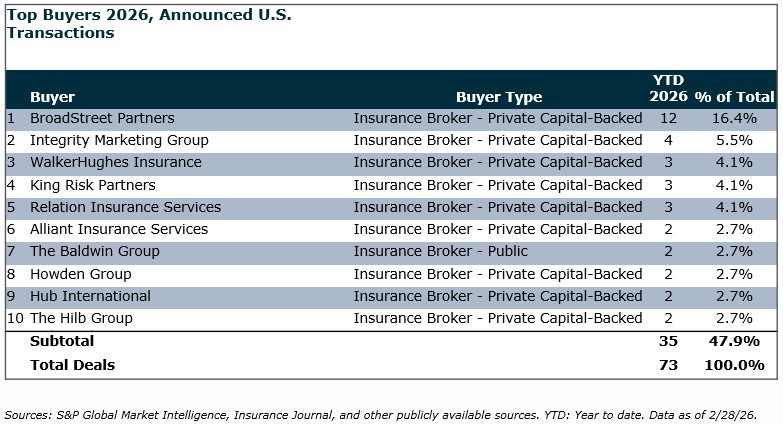

As of February 28, 2026, there were 73 announced M&A transactions in the U.S. This is down 14.0% compared to last year at this time when there were 86 transactions announced through February. This is likely to be due to delays in announcements and not a true reduction in activity. Private capital-backed buyers accounted for 47 of the 73 deals (64.4%) through February. Independent brokers were buyers in 13 deals so far in 2026, representing 17.8% of the market. Bank buyers announced two transactions YTD. Deals involving specialty intermediaries as targets accounted for 24 transactions representing 32.9% of all deals so far – a significant uptick in activity for a sector of sellers that has been in low supply for a few years.

Deal activity from the top ten buyers accounted for 47.9% of all announced transactions, while the top three (BroadStreet Partners, Integrity Marketing Group, and WalkerHughes Insurance) accounted for 26.0% of the 73 total transactions.

Notable transactions:

- February 10: Revau acquired Triad Oilfield Underwriters, a Houston-based managing general agent and wholesale brokerage specializing in upstream oil and gas and marine risks. Founded in 2017 and later expanded through a merger with Bayshore Underwriters, Triad operates as a Lloyd’s coverholder with delegated underwriting authority and maintains established relationships with specialty capacity providers, while also supporting retail brokers through a focused wholesale platform. The transaction strengthens Revau’s North American footprint by expanding its technical underwriting and placement capabilities in complex energy and marine sectors, aligning with its strategy to build a diversified, technology-enabled MGA platform. MarshBerry served as an advisor to Triad on this transaction.

- February 23: The Vistria Group acquired Lumen Holdings, a Dallas-based, technology-enabled managing general agent, establishing it as a new platform investment within Vistria’s financial services strategy. Founded in 2019, Lumen underwrites a diversified portfolio of commercial property, builders’ risk, general liability, personal auto, homeowners, and umbrella products across more than 30 states, supported by a nationwide network of wholesale and retail broker relationships. The transaction reflects Vistria’s focus on backing specialized MGAs with data-driven infrastructure and strong underwriting discipline, positioning Lumen for continued expansion through talent recruitment, program growth, and enhanced technology capabilities. MarshBerry served as an advisor to The Vistria Group on this transaction.