Insurance markets move in cycles, much like the seasons. For the past several years, it’s been in a hard market – a period where premiums rise and underwriting gets tighter. Recently, though, the climate has started to shift. Premium increases are slowing, and margins are thinning. Commercial lines premiums in Q4 2025 rose by an average of just 0.2%, down from 1.6% in Q3 2025.1 Even commercial auto, which previously had 58 straight quarters of increases, saw premiums decrease at the end of 2025. As the market shifts, agencies must consider new strategies to help increase organic growth in an evolving climate. After largely focusing on business retention, agents who shift from a retention mindset to a growth mindset will win.

How Insurance Market conditions have shifted

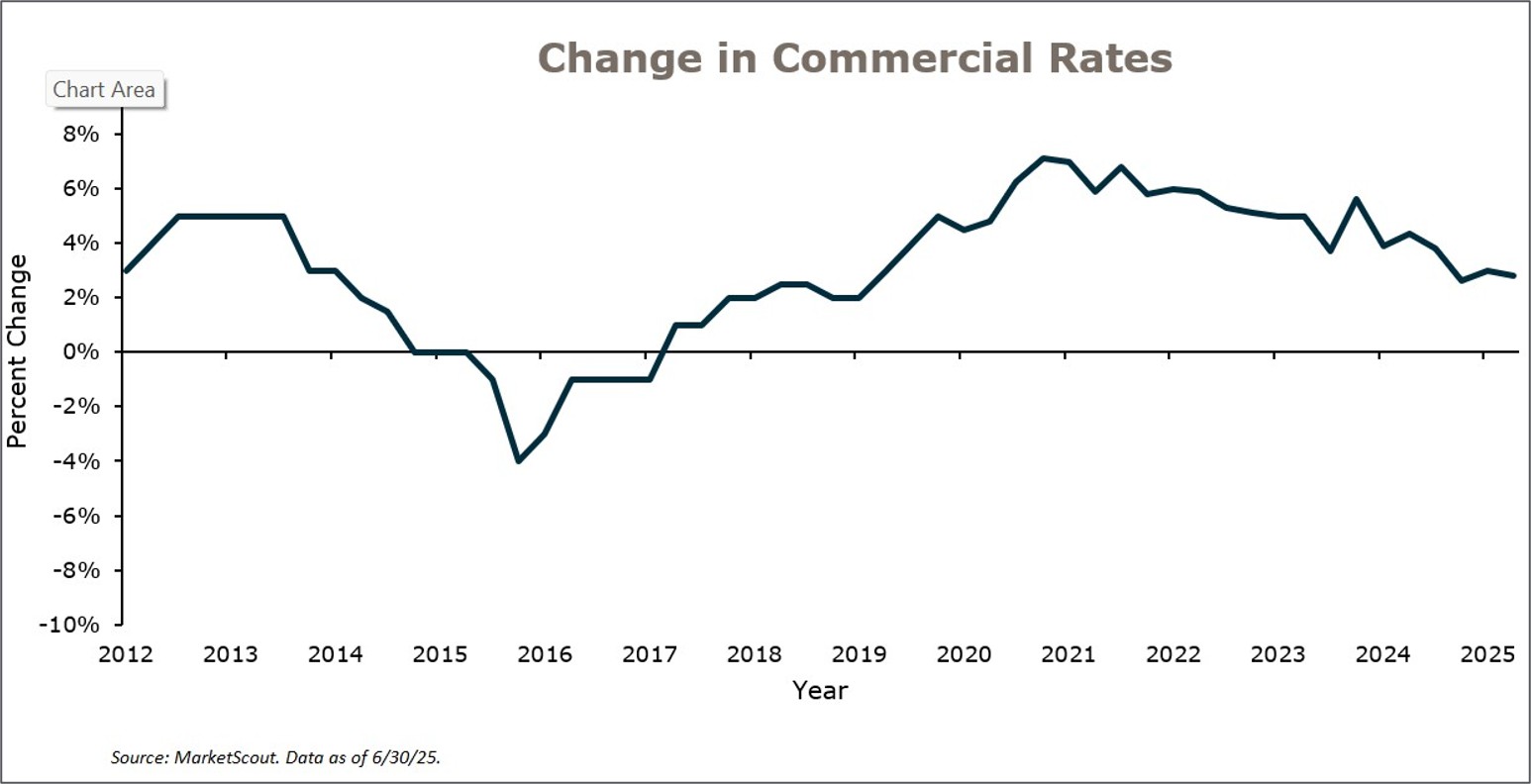

It is estimated that the insurance brokerage industry has been in a hard market for the last 6-8 years. MarshBerry defines a hard market as a period where product premium rates increase by over 5% for two or more years. Experientially, a hard market period is characterized by increased premium rates, restricted coverage, and lower capacity – caused by an increase in demand and decrease in supply of policies.

Market cycles are often subjective, and they rarely reflect conditions across all insurance lines. For example, while commercial property lines are clearly softening, casualty lines pricing continues to rise. Auto insurance rates are expected to rise in 2026, just at a slower pace. Overall, rate increases in commercial lines have been declining for roughly five years, from approximately 7% to roughly 3% by the end of 2025.

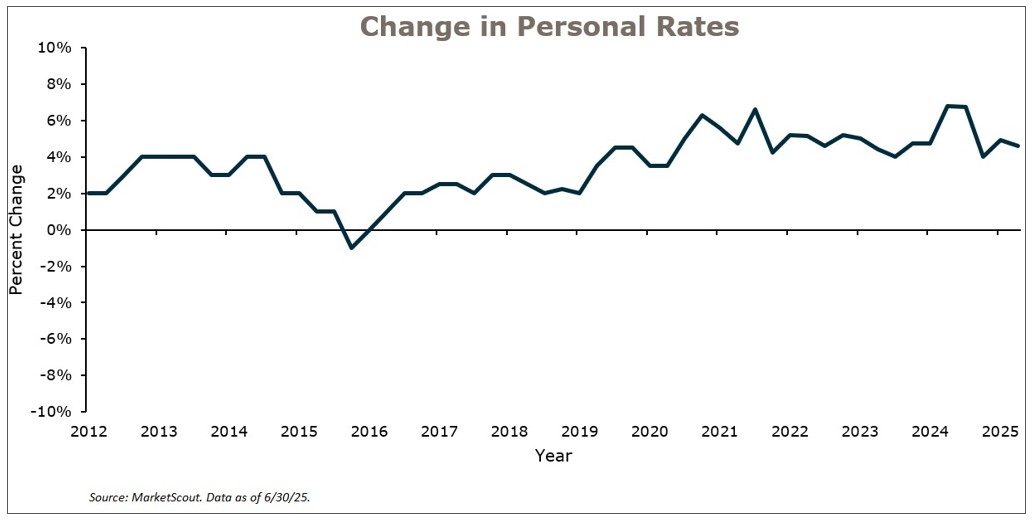

Rate increases in personal lines slowed on and off over the past five years, but when you add in inflation and exposure increases, some customers have seen significant double digits. In 2024, personal line rate increases hovered between 4-6%. These rate increases are expected to be steady or inflationary in 2026, depending on the lines and location of the customer. Some major personal auto insurance carriers are even beginning to decrease rates or slow the pace of hikes, particularly in states that have become highly profitable due to previous rate hikes and legal reforms.

Why Insurance Agencies Should Avoid the retention mindset

It’s natural that during a hard market, agencies will operate from a retention mindset, including overlooking weekly and monthly sales goals, focusing more on current client relationships, and prioritizing those accounts over new business.

But as the market grows softer, carriers will be seeking growth opportunities. Many have taken rate decreases, like in personal auto, to become more competitive. As supply outpaces demand, agencies should pivot to hunting for new clients. It’s a good time to dust off old marketing strategies and get proactive with clients to understand their evolving needs. Lower prices mean clients become more receptive to recommendations, so it’s a prime time to encourage them to add new services or lines of coverage. Soft conditions are also optimal for attracting new clients due to more favorable conditions for buyers, particularly those who wanted to purchase more coverage but either couldn’t afford it during a hard market or were previously denied coverage. Growth won’t come from premium increases, so it needs to come from new clients.

Opportunities for agencies who shift to a growth mindset

As premium rate increases slow, agencies may see some pressure on their commission earnings. Competition may expand, creating challenges around client retention. Because rate increases will be less of a factor in fueling growth, agencies that have a mindset of focusing on getting new customers will have a competitive advantage. Ways to shift to a growth mindset include:

- Set clear goals and expectations. Ensure producers have a new business revenue goal, one that is challenging, yet realistic. If they brought in $80,000 last year maybe aim for $100,000 this year. Besides a lag indicator (like new annual commissions), what lead expectations do they have for number of calls, appointments, quotes and binds by market segments? Use outside resources that can provide benchmarking for your producers’ performance, like a Producer Stack Ranking.

- Be proactive, not reactive in client relationships. Call your clients and educate them on what’s happening in the markets, including how you plan to support them. Coach your staff on how to differentiate your value proposition. Remember that as an independent agency, you’re a trusted advisor. Communicate like one.

- Implement technology solutions. Competition for the independent insurance agency is fierce, but investing in advantageous technology (such as AI tools) is one way to get ahead. The right tools can help optimize efficiencies, drive sustainable growth, and create business intelligence that enhances your agency’s evolution.

- Explore new business niches and become a specialist: What does your agency do better than any other agency? Do you have a specific passion towards a particular class of business? Being a trusted advisor, as opposed to just a vendor, can differentiate an agency from its competition. Clients may see more value when they are offered prescriptive solutions that help with risk mitigation.

- Sell more commercial. Diversity in an agency is key and allows for the opportunity to pivot regardless of the market. Businesses need insurance to operate so there are many opportunities for producers to uncover more predictable income. As producers grow their book, hire additional service people to free up their time to continue to do what they do best – produce.

- Invest in producers by prioritizing training and development. If your agency conducts an annual sales kickoff, how much do you focus on training? Training and developing producers should be a core part of your culture. Start by looking at the team’s weak spots and create a “practice” plan around improving those weak spots. The best sports teams practice daily, shouldn’t your sales team do the same? Remember that it’s not just about understanding insurance products and markets. Producers should be focused on how to articulate your offer in a way that’s specific to the client’s needs.

Now is the time to get aggressive and fight to stay competitive. Many carriers are focused on growth and are demonstrating greater flexibility to secure new business. They are often more open to offering enhanced policy limits and more favorable terms, providing agencies with greater ability to tailor coverage to the unique needs of their clients. This level of market openness has not been seen in several years, so now is the time to get after it.