M&A market update

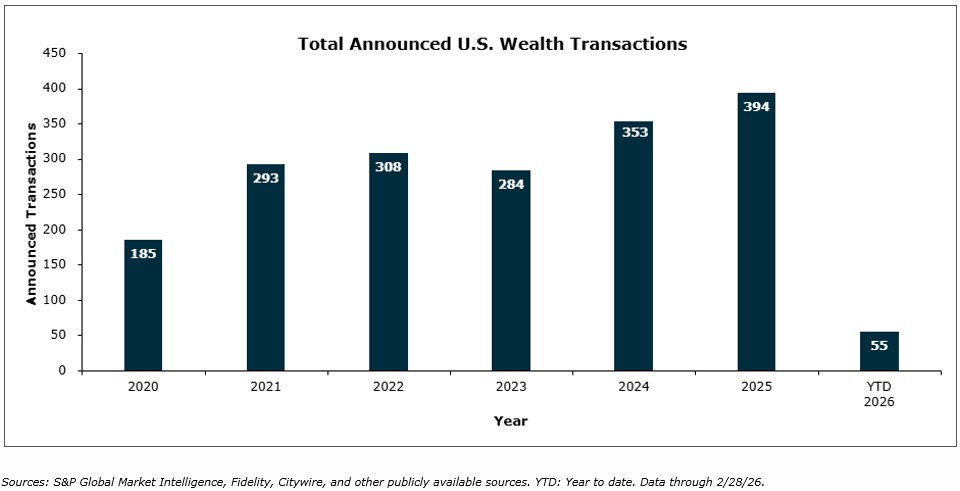

Through the first two months of 2026 there have been 55 wealth management merger and acquisition (M&A) transactions announced in the U.S. This represents an 8.3% decline from the 60 deals recorded over the same period in 2025, but 14.5% higher than the same point in 2024.

Private capital-backed buyers continued to set the pace through February, completing 38 of the 55 announced transactions and representing 69.1% of total activity. Independent acquirers accounted for 13 deals, or 23.6% of the market, while insurance brokerages completed three acquisitions during February.

The top 10 buyers represented 43.6% of total transactions, and the top three acquirers (Hightower, CapTrust, and Mercer) accounted for 18.2% of all announced deals. At the same time, geographic dispersion reinforces the breadth of the current market environment. A total of 28 states recorded wealth management M&A activity through February, with California leading the country at five transactions, underscoring both the depth and national reach of ongoing consolidation.

Capital remains abundant, with both financial and strategic acquirers actively pursuing high quality platforms and add-ons. Given that transactions often reflect processes launched months or even more than a year prior to closing, short-term market headlines or geopolitical developments typically have a delayed impact on reported deal activity.

At the same time, broader market volatility is prompting firm owners to think more strategically about growth and resilience. Many are evaluating how well positioned they are to sustain a market correction or prolonged flattening, particularly if organic growth has historically relied heavily on referrals. Rather than moving to the sidelines, this environment is pushing firms to consider partnerships that can strengthen business development capabilities and provide additional infrastructure. The long-term drivers of registered investment advisor (RIA) consolidation, including demographics, succession planning, scale economics, and institutional capital, remain firmly intact.

Private equity (PE) interest continues to be a meaningful force, with ten distinct direct PE investments already announced in 2026. Notably, AI is increasingly serving as a catalyst for transactions rather than a deterrent, as firm owners recognize that keeping pace with technological change and cybersecurity demands requires scale, sophistication, and access to capital.

Notable transactions:

February 11: Aerodigm Wealth launched in Portland, Oregon, following a management buyout of the wealth advisory division of Delap LLP, establishing a new tax-focused registered investment advisor overseeing approximately $1.5 billion in assets as of year-end 2025. Led by Jared Siegel and joined by longtime Delap principal Dave DeLap, the firm will focus on ultra-high-net-worth individuals and families, integrating tax-aware portfolio construction and multigenerational planning while coordinating closely with clients’ external tax professionals. The launch follows the sale of Delap’s accounting and consulting business to Aprio and reflects a broader industry trend of RIAs leaning into tax-efficient wealth strategies, particularly for clients in high-tax jurisdictions. Aerodigm intends to scale nationally, positioning tax strategy as a core driver of long-term, risk-adjusted wealth outcomes.

February 26: OneDigital acquired Silicon Valley Retirement Services and Derse Morgan Financial Advisors, adding a combined $1.73 billion in client assets to its wealth and retirement platform. Silicon Valley Retirement Services, based in San Jose, specializes in fiduciary advisory, plan administration, and participant education for retirement plans, strengthening OneDigital’s presence in Northern California. Derse Morgan, headquartered in North Carolina, focuses on financial planning and investment advisory services for individuals and corporate executives across multiple industries. The transactions mark OneDigital’s first wealth and retirement acquisitions of 2026 and build on its strategy to integrate retirement plan advisory with broader wealth management capabilities.

Looking forward

The wealth management M&A market in 2026 maintains constructive underlying conditions. Valuations remain strong, the buyer universe is deep and increasingly experienced, and private capital continues to show sustained interest. As firms evaluate strategic options, timing is only one part of the equation. Increasingly, owners are approaching potential transactions with a clearer focus on long term objectives, leadership continuity, and how a partnership may support future growth and investment.

While near term deal counts may fluctuate, the broader consolidation narrative across wealth management remains intact. Firms continue to seek scale, expanded capabilities, and long-term partners that can support the next phase of industry competition. With capital available and buyer appetite steady, the environment remains supportive for well positioned firms considering strategic transactions.