At the moment, specialty intermediaries — particularly those operating in excess and surplus (E&S) and delegated authority markets — are commanding historically high valuations. Behind this headline lies a deeper story about the dynamics of capital markets and the evolving economics of the specialty sector. Understanding these dynamics is critical for firms seeking to remain competitive in the years ahead.

The growing importance of scale

In today’s specialty marketplace, scale increasingly determines relevance. MarshBerry estimates that by the end of 2025 there were 27 property and casualty (P&C) specialty platforms based in the U.S. with more than $1 billion in premium, controlling roughly three-quarters of the $230 billion (estimated) of specialty premium placed last year. Reaching that level of scale typically reflects several structural advantages:

- Diversification in a segment where independent operators are prone to concentration risks

- Ability to attract, develop and retain top caliber talent

- Capabilities, systems, processes, and leadership positioned for further growth

- Growing clout among carriers, distribution partners, vendors, etc.

These capabilities allow large platforms to shape the marketplace, not simply participate in it, and drive value to stakeholders. Meanwhile, smaller (typically independent) operators — even those growing at strong rates — can gradually lose relative influence as scale consolidates among the largest platforms.

A shift in growth strategies

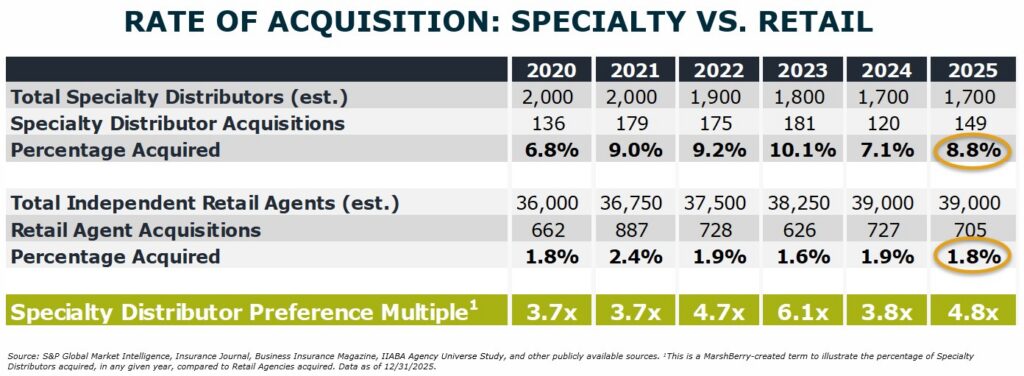

Historically, organic (i.e. rate and exposure base change) and inorganic growth through acquisitions were dominant strategies in specialty. But this approach is becoming increasingly difficult to execute. On the organic growth front, we are generally entering a softening (soft for certain lines such as cat exposed property) market after an unprecedently long half-decade, firm-to-hardening cycle. Shifting to inorganic growth, in 2025 alone, approximately 149 transactions occurred across an estimated 1,700 specialty firms, meaning nearly 9% of the sector consolidated in a single year. That compares to retail brokers’ consolidation at less than 2%.

As acquisition opportunities become scarcer — and valuations rise — most large specialty platforms have pivoted growth strategies to capitalize on underwriter and broker recruiting. This is oftentimes referred to as “incubation” in the marketplace, where a platform may recruit underwriting talent and offer them back-office services while the underwriter/team establishes and grows a program. Incubation has become particularly attractive because it allows firms to build new platforms at a fraction of the cost of acquiring an established intermediary while controlling areas of focus (e.g. lines of business and/or coverage type) and cultural/operational characteristics valued by the platform.

Why specialty has become the industry’s growth engine

Over the past 15 years, specialty insurance has grown significantly faster than traditional retail brokerage. During that period, retail premium growth averaged roughly 4.6% annually, while specialty premium growth approached 12%. Several structural characteristics help explain this divergence. Specialty intermediaries typically focus on niche markets where expertise and underwriting insight may create differentiation for carriers looking to delegate underwriting authority and distribution partners seeking a unique risk-mitigation solution. These dynamics have resulted in testing and repositioning of traditional industry standards. For instance, delegated authority firms almost always operate with leaner cost structures and greater operational agility than traditional carriers. This has encouraged risk takers to leverage the delegated authority segment as they seek to grow quicker than they would likely be able to alone. As a result of these characteristics (and others), MGAs and delegated authority platforms have become increasingly valuable partners for carriers — enabling rapid adaptation to emerging risks and market opportunities.

The “golden age” of delegated authority

Within the broader specialty ecosystem, one segment has attracted exceptional investor interest: delegated authority platforms. In recent years, delegated authority platforms have commanded record valuations. Private equity investors are currently paying higher valuations for delegated authority platforms than strategic buyers! This is very unusual as strategic buyers generally are able to leverage synergies from a potential transaction. These synergies do not exist when a financial sponsor makes an initial capital outlay into a platform. Why is this occurring? The driver is scarcity. Put simply, there are relatively few scaled delegated authority platforms capable of serving as the foundation for the next generation of billion-dollar premium specialty intermediaries. As capital continues to pursue these opportunities, valuations have climbed to unprecedented levels.

Key takeaways

Despite the sector’s momentum, the next phase of the market cycle may create challenges. Several trends contribute to this dynamic:

- A half decade of rate tailwinds are turning into headwinds.

- Large retail brokers continue expanding their wholesale and specialty capabilities.

- Competition for underwriting talent increasingly favors scaled platforms (putting more pressure on independent operators).

- Technology investments by large specialty platforms continue to widen the relevancy gap with that of smaller operators.

Capital inflows, strong premium growth, and limited supply of scaled platforms have combined to create extraordinary demand in the specialty area. Firms that demonstrate niche expertise with strong value-add propositions and incubation of underwriting talent will continue to have the greatest growth prospects and therefore continue to drive premium valuations in the market.