Everything in the world is changing – and it is changing faster than ever. The geopolitical landscape, macroeconomic conditions, global conflict, climate risk, technology, and specifically AI – are all evolving at a staggering pace. These shifts are no longer operating independently; they are deeply interconnected and collectively influencing financial, operational, and strategic decisions for businesses and individuals alike.

At the center of this complex web sits the insurance brokerage industry. Insurance brokers assess risk, translate uncertainty, and provide protection in an environment where volatility has become the norm rather than the exception. Yet while brokers help clients manage change, the industry itself is being reshaped by these factors at an unprecedented rate. In fact, this industry has shifted from what was once just considered a “landscape of uncertainty” to one that is now seen as the “exponential momentum of uncertainty.”

What that means is, the biggest threat to insurance brokers isn’t any single disruption like AI, the consolidation of this industry, or a soft rate environment – it’s clock speed. It’s the exponential momentum of uncertainty and the rate of change which is compounding faster than most firms’ ability to adapt.

In this rapidly changing environment, every leader must ask a critical question: What is our firm’s clock speed? Working harder and working smarter is no longer enough. Firms are now facing the necessity to work faster to keep up with this rate of change. They need to determine whether the firm is evolving fast enough to keep pace with external forces.

The uncomfortable truth is: firms that fail to adapt their clock speed to the rate of change surrounding them will fall behind quickly. And when a firm fails to keep pace, valuation will inevitably suffer.

The race for scale

Looking back over the past 15 years, the insurance brokerage industry has experienced unprecedented consolidation. M&A activity accelerated rapidly following the global financial crisis, driven largely by private equity (PE) firms attracted to strong cash flows, recurring revenue, and resilient long‑term demand.

During this time, the influx of capital sparked a feeding frenzy. Valuations expanded, deal multiples increased, and buy and build platform strategies became the dominant growth model. Scale became synonymous with value, and for good reason. Larger firms benefited from broader market access, deeper resources, enhanced remuneration with carriers, and improved operating leverage.

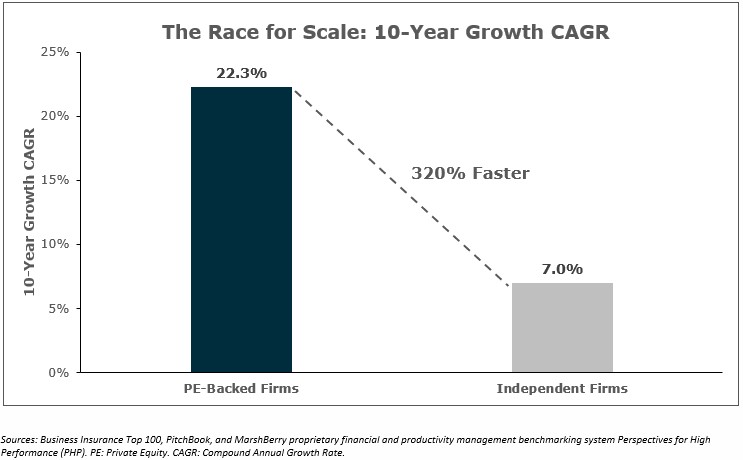

Today, PE-backed brokers are growing at over 320% faster than independent firms. Scale is no longer optional – it’s a critical strategy for remaining in control of your future.

But scale is no longer a differentiator on its own. Many firms that grew aggressively through acquisitions now face the reality that integration, organic growth, and productivity matter just as much – if not more – than deal volume.

Firms that continue to operate as they did in the past are quickly discovering that yesterday’s playbook no longer works. The past can no longer reliably predict the future.

A new landscape defined by clock speed

While brokers are experiencing the rate of change from external factors, they also face increased structural challenges from within the industry. Pricing momentum is softening after several years of tailwinds, impacting organic growth across all firms – public, private capital-backed, and independent brokers. At the same time, leverage ratios have crept higher, integration discipline has become a critical determinant of M&A success, and there is severe competition for talent – with employee lift‑outs becoming part of the growth strategy for many large brokers.

Finally, technology – and especially AI – is accelerating the rate of change in this industry even further. AI is not a distant future concept – it is here, already reshaping underwriting, service models, data analytics, and client expectations.

All of this creates a fundamental tension: while risk is increasing and becoming more complex, the traditional methods brokers used to drive growth and value are proving less effective.

Organic growth and valuations

After several years of favorable pricing conditions, the market has begun to soften, limiting organic lift from rate increases and revealing structural growth weaknesses in many firms.

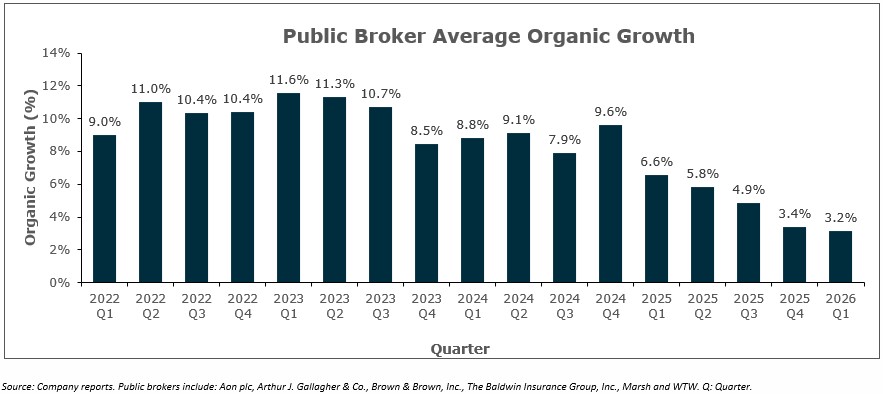

The public brokers have suffered more than the broader market given their greater concentration in larger accounts and Excess and Surplus (E&S) property, areas under more competitive pressure compared to smaller accounts. Organic growth for public brokers has dropped significantly, from averaging 10.5% in 2023 and 5.2% in 2025 to a three-year low of 3.2% in the first quarter of 2026.

In addition to a softening market and slowing organic growth, the public brokers in 2026 have also seen a sharp decline in stock prices – the result of investor concerns that conversational AI is moving closer to the point of sale in the insurance distribution chain. (See Is AI Rewriting The Rules of Insurance Distribution?)

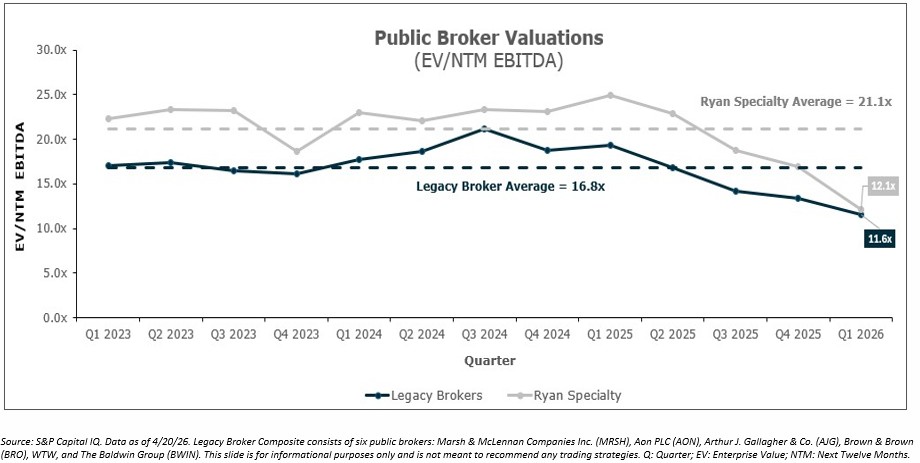

All of these factors are beginning to weigh on the valuations of the six public brokers. After peaking in 2024, reaching 20x EBITDA (earnings before interest, taxes, depreciation and amortization), public broker multiples declined in early 2025 and now trade at a median of approximately 12x EBITDA. This decline reflects a combination of slowing organic growth, concerns about a softer pricing cycle, and uncertainty around AI’s long‑term impact.

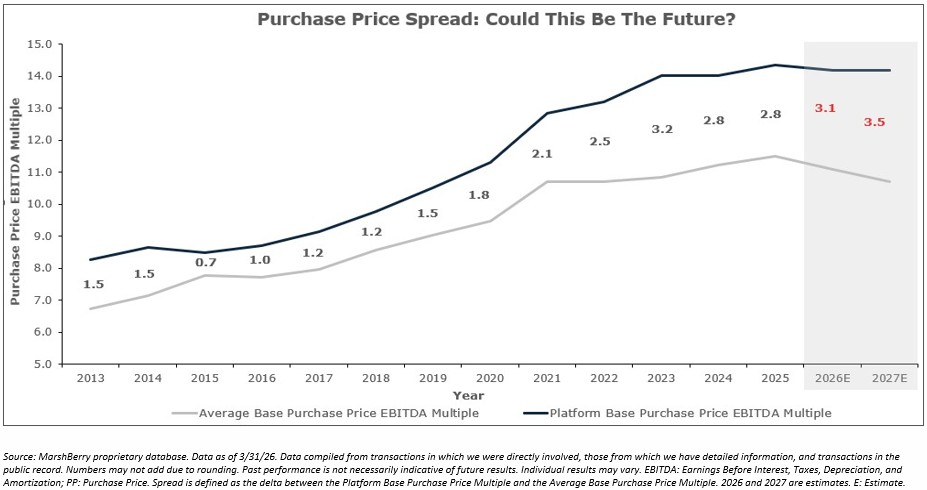

In contrast, valuations for privately held platform brokers have remained more stable. The reason private broker valuations have not mirrored the public market’s decline is the same reason they did not spike when public valuations surged in 2024. Public market valuations are driven heavily by investor sentiment, while private broker valuations are driven primarily by performance.

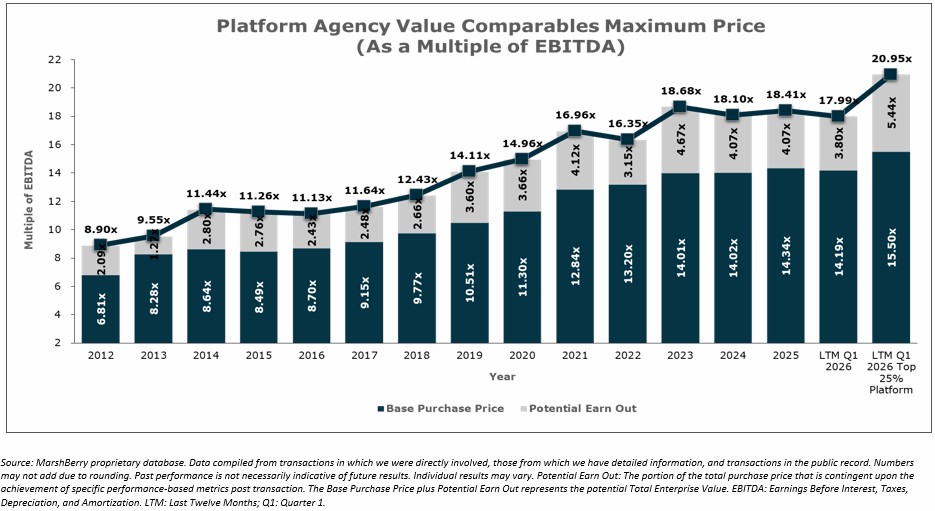

Over the past three years, private platform firms have held flat at an average of around 14x EBITDA for base purchase price at closing and near 19x with an earn-out. MarshBerry does not predict a significant multiple contraction for private brokers as demand continues to significantly outstrip supply.

That said, buyers are becoming more selective. MarshBerry expects increased separation between “average” firm valuations and true platform valuations. Firms that bring scale, specialization, technology readiness, and organic growth discipline will command premium valuations. Others may struggle to maintain elevated multiples.

Is AI rewriting the rules of insurance distribution?

AI is accelerating the clock speed even further and is now firmly on the radar of every insurance industry executive. There is growing debate about whether AI’s emergence is a “canary in the coal mine” for the brokerage model, particularly as public broker valuations have declined. The real story, however, is more nuanced. AI is not eliminating the need for brokers. Instead, it is rewriting the rules of competition.

We believe that AI’s ability to drive efficiency, speed, and scalability will benefit the insurance industry. It will automate routine tasks, enhance data-driven insights, and free up human capital for higher‑value advisory work. In doing so, it will create more capacity – which ultimately leads to more growth potential.

Perhaps most importantly, AI will dramatically increase the volume and sophistication of curated solutions by industry vertical, as brokers will be able to design more targeted, proactive risk mitigation strategies that address evolving safety, regulatory, and operational risks. As a result, client expectations will rise – and that is where the point of differentiation will occur.

Larger, more sophisticated brokers that invest meaningfully in AI will be able to accelerate organic growth through the efficiency and speed which AI provides. The resulting increase in operational capacity will allow them to onboard more clients, deepen relationships, and retain accounts more effectively.

Smaller brokers that cannot keep pace with technology investment will feel the inverse effect. As efficiency gaps widen, these firms will struggle to meet client expectations, slowing growth and ultimately impacting valuations.

AI may not meaningfully expand margins for leading firms as increased efficiency will be redirected toward driving value proposition and in turn organic growth. As a result, it will raise the bar for the entire industry. This is simply the next chapter in the insurance brokerage arms race – with technology becoming a core component of the value proposition.

How brokers can reset their clock speed

Despite this new clock speed, the rate of change, and current headwinds, consolidation in this industry shows no signs of stopping. Capital remains abundant, and strategic buyers still see insurance distribution as a compelling long-term investment.

However, the nature of consolidation is changing. Acquirers are scrutinizing organic growth, producer productivity, leadership depth, and integration readiness more than ever. Simply being available is no longer enough to command top-tier value. Firms that can’t generate competitive levels of organic growth in this softer rate environment are going to be less attractive to potential M&A acquirers and even risk being left behind in the race for scale. To remain competitive and attractive, brokers must take deliberate action. Key priorities for firms looking to increase their clock speed include:

- Improve sales velocity. New business output per producer remains low across much of the industry. Firms must enhance sales discipline, accountability, and enablement to drive greater productivity from existing teams.

- Invest in the next generation. Many organizations underinvest in developing future producers. Low Net Unvalidated Producer Pay (NUPP) ratios signal risk to long‑term growth. Sustainable firms commit capital and mentorship to building tomorrow’s revenue engine.

- Optimize equity structures. Lowering a firm’s Weighted Average Shareholder Value (WASA) has consistently been shown to improve profitability and enhance attractiveness to potential acquirers.

- Specialize. The days of being everything to everyone are fading. Specialization allows firms to deliver more relevant solutions, command higher perceived value, and stand out in competitive M&A processes.

- Invest in technology. Technology investment is no longer optional. AI, data analytics, and workflow automation create efficiencies, improve client outcomes, and unlock capacity for additional growth.

- Become a trusted advisor. Brokers that transition from transactional sellers to trusted advisors help clients reduce risk exposure and claims severity – deepening relationships and driving retention.

Final thoughts

The insurance brokerage industry stands at a pivotal moment. The clock speed has accelerated across every dimension – economic, geopolitical, technological, and competitive.

Firms that recognize this shift and adapt accordingly will continue to thrive, grow, and create value. We believe those that rely on past success as a predictor of future results will find themselves falling behind faster than they expect.

In an industry built around understanding risk, the greatest risk brokers face today may be failing to evolve quickly enough. The question every broker must answer is simple: Is your firm’s clock speed sufficient for the landscape of risk ahead?