For wealth management firms, the past decade and a half has been extraordinary: advisory businesses have benefited from one of the strongest economic expansions since the Great Depression; equity markets have surged; client assets have grown; and firm valuations have climbed dramatically as multiples for wealth management firms more than doubled. What was once a relatively quiet corner of financial services has now emerged as one of the most attractive asset classes in the global investment marketplace.

Institutional investors recognize the durability of the advisory model – strong recurring revenue based on deeply embedded, long-term client relationships, strong EBITDA (earnings before interest, taxes, depreciation and amortization) margins, and a fragmented market in which thousands of independent firms remain potential acquisition targets. The result has been an influx of capital and unprecedented interest in the sector.

The rapid acceleration of mergers and acquisitions (M&A), fueled largely by private capital, is reshaping wealth management’s competitive landscape. For firm owners, the environment now presents both tremendous opportunity and mounting pressure.

A tidal wave of capital

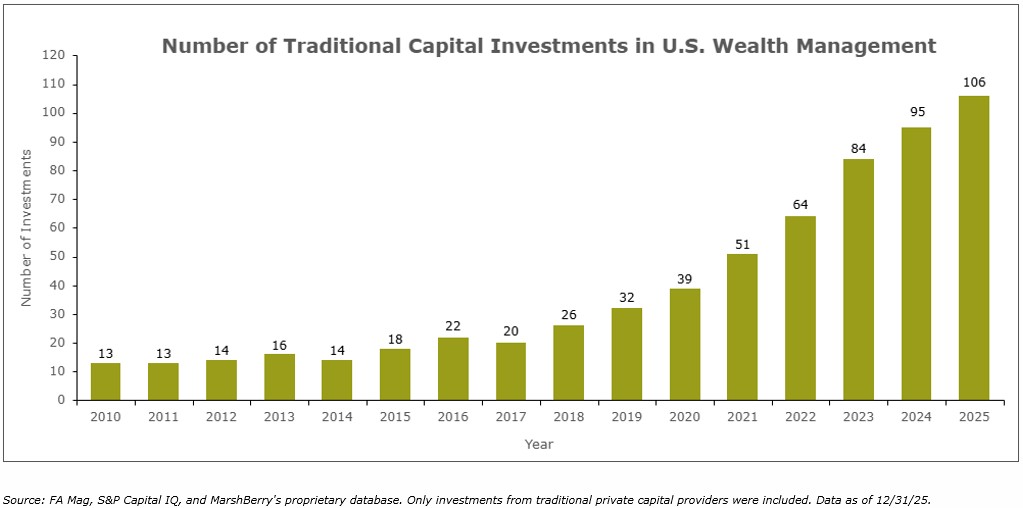

M&A activity within wealth management has reached levels few industry veterans would have predicted a decade ago. Transactions have multiplied as investors increasingly view advisory firms as scalable platforms capable of generating attractive long-term returns.

Private capital, in particular, has played a significant role in driving this transformation as private equity (PE) firms have come to recognize that wealth advisory presents relatively low capital intensity with basically zero, large physical assets or heavy infrastructure investments, all of which translates into substantial free cash flow. In addition, the wealth management model aligns well with the investment thesis of many PE firms. Investors typically seek businesses capable of generating a three times multiple of invested capital in five years (3x MoIC), which translates to average annual returns of approximately 25% over a multi-year investment horizon. The advisory sector offers a path to achieving those returns through a combination of organic growth, acquisitions, operational improvements, and financial leverage.

A race for scale

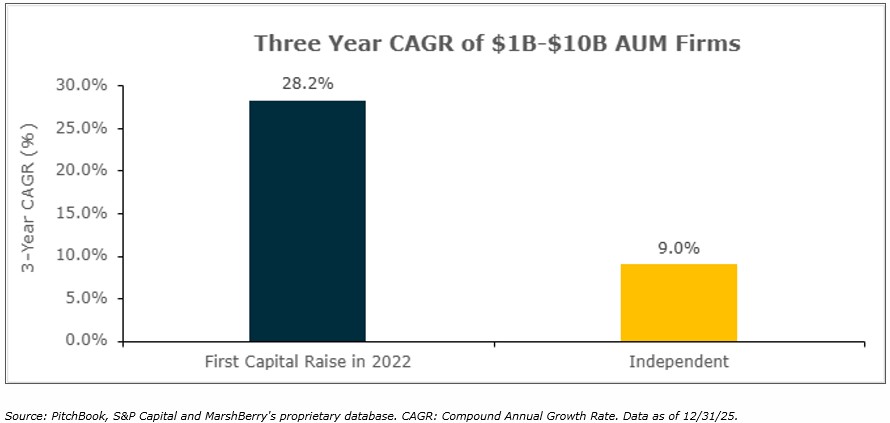

The industry’s attractiveness has created what can only be described as a race for scale. Buyers are seeking to grow rapidly through acquisitions, building larger advisory platforms capable of offering broader services, deeper resources, and enhanced technology. In many cases, the size of leading firms has expanded almost exponentially as consolidation accelerates across the industry. This, in turn, has had a dramatically positive effect on their ability to generate a better compound annual growth rate (CAGR) in assets under management, revenue, EBITDA and enterprise value.

As a result, smaller independent firms increasingly find themselves facing the threat of being quickly marginalized as they compete against organizations with greater resources.

Why firms are choosing to sell to (or buy into) a third party

Against this backdrop, many firm owners are choosing to partner with larger platforms or PE investors. Several factors help explain why:

- Scale increasingly influences a firm’s ability to attract and retain talent. High-growth platforms often provide clearer career paths, stronger recruiting capabilities, and more robust equity incentives for advisors and leadership teams.

- Client expectations continue to expand. Wealth management is evolving beyond traditional investment advisory services – toward a more comprehensive financial ecosystem. Larger firms are investing heavily in capabilities such as tax planning, estate coordination, family office services, insurance advisory, and more, all while implementing advanced technology platforms designed to enhance client experience. For many independent firms, building these capabilities internally can prove expensive and operationally complex. By joining a larger platform, independent firms can gain access to those resources almost instantly.

- Advancements in artificial intelligence are accelerating rapidly. These investments have the potential to transform the industry by driving meaningful operational efficiencies, enhancing client service and experience, and enabling advisors to focus more on clients rather than administrative processes.

- Financial incentives are too compelling. Most PE-backed buyers allow sellers to monetize a significant portion of their equity while retaining a minority stake in the larger enterprise. In some cases, that minority stake has generated substantial additional value as the platform continues to grow – sometimes even surpassing the amount received for the original equity stake. These dynamics have helped transform what was once a relatively uncommon transaction into a mainstream strategic decision for wealth advisory owners across the industry.

The strategic decision facing firm owners

For wealth management leaders, these market dynamics ultimately lead to a fundamental strategic question: What role does the firm intend to play in the future landscape of the industry? Broadly speaking, firms face three potential paths forward:

- Sell the business to (or buy into) a third party. Some owners will determine that the current market represents an attractive opportunity to monetize their equity while partnering with a larger organization capable of supporting continued growth.

- Maintain the status quo. Other firms may elect to operate as lifestyle businesses, prioritizing steady income and long-term client relationships rather than intentional expansion. These businesses are, in effect, selling their business over time, extracting earnings and consuming enterprise value versus reinvesting earnings to drive enterprise value.

- Invest in growth. Some will choose to compete actively in the evolving marketplace by reinvesting in talent, technology, and service capabilities. These firms aim to strengthen their competitive position and remain independent while continuing to build long-term enterprise value.

Each option can be viable depending on the firm’s goals, leadership structure, and appetite for growth. However, firms that intend to remain independent must recognize that the competitive bar is rising rapidly and maintaining the status quo may not be viable over the long-term.

The blueprint for growth

Sustained organic growth has become one of the most important differentiators between firms that thrive and those that struggle. In many cases, market performance has masked the true underlying growth of advisory businesses. Rising equity markets have increased client assets across the board, making it difficult to distinguish between firms benefiting from market tailwinds and those that are genuinely generating new business. This is why investors and acquirers increasingly focus on market-adjusted growth – the ability to bring in new client assets independent of market movement. Firms that consistently generate meaningful organic growth are typically viewed as stronger long-term investments. Achieving that level of growth requires intentional strategy, and high-performing firms often adopt several common practices:

- Clear accountability for business development

- Defined roles for advisors responsible for new client acquisition

- Measurement of new assets as a percentage of existing assets under management

- Incentive structures that align advisor compensation with firm growth

These mechanisms help ensure that growth is driven by strategy rather than by favorable market conditions.

A pivotal moment for the industry

The wealth management industry remains in a powerful expansion phase. Capital continues to flow into the sector, and demand for advisory services remains strong. This is good news for independent wealth advisory owners, but it also means that the forces reshaping the industry – consolidation, scale, and institutional investment – are unlikely to reverse. For firm owners, the key question is not whether change will occur, but how to respond. Those who approach the future deliberately, whether by selling, or strategically growing, will be far better positioned to navigate the next chapter of the industry’s evolution. In a market defined by rapid transformation, strategic clarity may prove to be the most valuable asset of all.